Many merchants are still operating with checkouts built around cards alone. Whilst cards remain a popular way to pay, these same merchants are watching potential customers abandon at checkout because their preferred way to pay isn’t available.

This aligns with changing consumer demands. Recent data has revealed that 60% of ecommerce transactions in Europe are now being made using alternative payment methods. This shift towards alternative payment methods (APMs) is outlined in our latest report, How Europe likes to pay: navigating emerging cross-border payment methods.

Wider data from the report confirms that consumer behaviour varies significantly from one country to the next — and the merchants who understand localised payment methods (LPMS) are quietly converting customers others are losing.

Every country has its own payment preferences

Across Europe, payments don't follow a uniform pattern or trend, with most countries choosing to accept payments their own way. In the Netherlands for example, iDEAL | Wero accounts for 73% of all online payments. And in Poland, BLIK has become the country's most-used ecommerce payment method, with nearly 20 million active users.

Spain tells a similar story. Bizum has 28.2 million active users supported by 38 banks. Meanwhile, in Portugal, 76% of online shoppers choose MB WAY when it's offered at checkout. Multibanco, a Portuguese interbank network, and MB WAY together account for roughly 80% of Portugal's ecommerce market.

Germany is also worth paying attention to for merchants. PayPal is the leader with 28% of online purchases in 2024, while Buy Now, Pay Later (BNPL) options account for 27% of ecommerce transactions and credit cards capture just 11%.

Looking holistically at the market, it’s clear that a one-size-fits-all checkout approach doesn't hold up across Europe. Merchants that place their efforts in high-performing countries and offer their preferred LPMs are seeing results where it matters.

What merchants are actually losing

Those that don't see a different side. When a customer lands on a checkout page and can't find a payment method they trust or regularly use, the most likely outcome is an abandoned card and a lost sale.

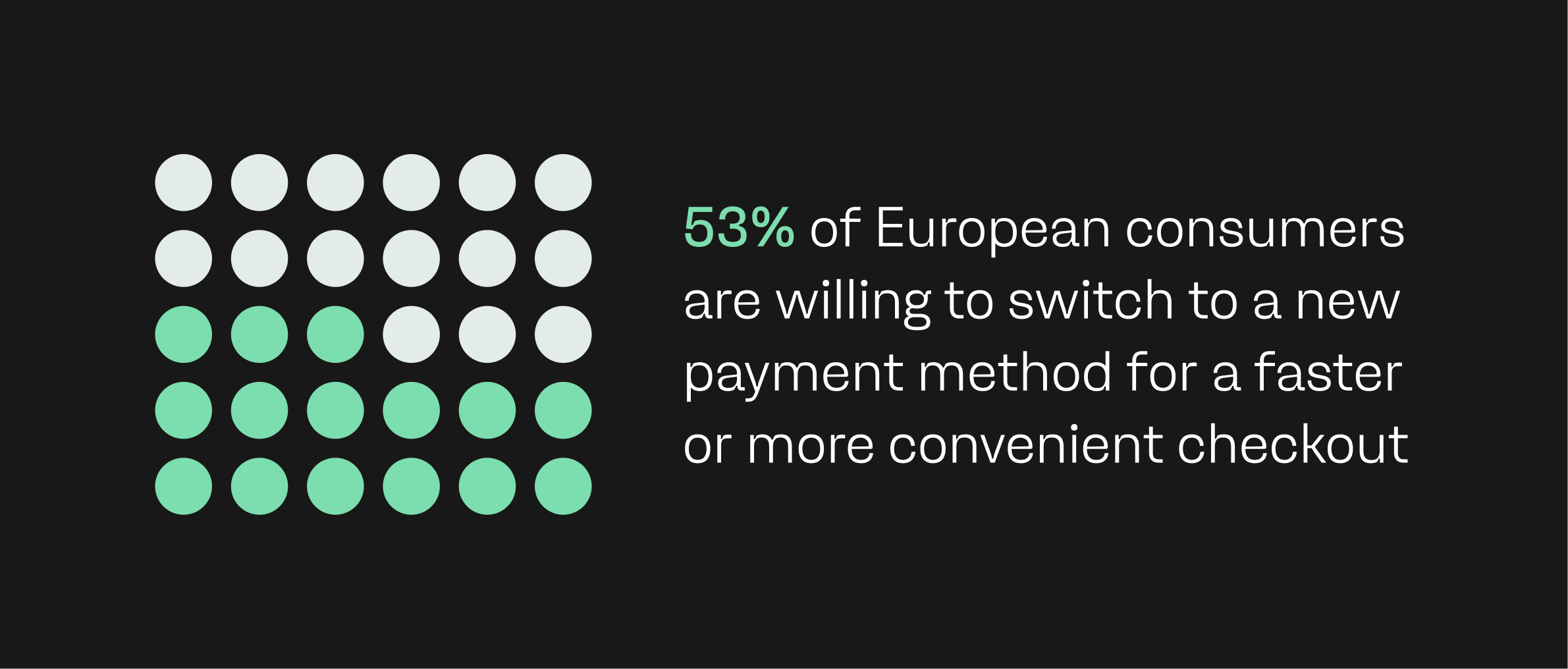

Data from the report shows that 53% of European consumers are willing to switch to a new payment method for a faster or more convenient checkout. However, this also means the reverse is true — when the experience falls short of expectations, carts are abandoned and sales are lost.

This cost to merchants is direct and hard-hitting, but there are ways to overcome these issues. For example, the report reveals that Integrating at least one APM produced a 12% revenue increase and a 7.4% increase in conversions. That's a significant return for a single integration.

As Marios Pitsillidis, APMs Operations Lead at payabl., notes in the report: "We're in a moment where adding a single payment method can genuinely move the needle for a business. Those who act on it are building a meaningful competitive advantage which compounds as they scale."

Local methods bring more than just convenience

There's a practical case for LPMs beyond checkout completion rates. Solutions like Wero, BLIK, Bizum, and MB WAY are bank-backed. This offers an inherent level of consumer trust that standalone digital wallets often can’t and don't provide.

Wero, for example, settles in 10 seconds and removes payment friction for 50 million existing users across key areas in Europe like Benelux and Netherlands. For merchants, that means faster cash flow and fewer hurdles between a customer's decision to buy and the payment being completed

The cost angle is also worth considering for merchants. Account-to-account (A2A) based LPMs like Wero offer transaction fees considerably lower than card interchange rates. The emergence of these Open Banking-powered solutions means fees tend to run lower (0.3%) than card fees, which run at roughly 1.5%-3.5%. At volume and scale, those savings add up.

Local and global should work together

Despite their upside, integrating LPMs doesn't mean removing cards or global schemes like Visa or Mastercard entirely. It means building a checkout that serves every customer and every need.

In general, the more options a customer sees, the more likely they are to find their preferred method and move forward with their purchase.

However, the key for merchants is being targeted rather than cluttered with your approach: identify your highest-performing markets and countries in Europe, find the dominant LPM in each, and make sure it's offered prominently alongside card schemes at checkout.

For merchants selling across multiple European territories, solutions like Wero are particularly useful. A single integration provides access to multiple territories, reducing the technical overhead of managing multiple local integrations.

The EuroPA alliance, which connects solutions like Bizum, MB WAY, Bancomat, and Vipps MobilePay, is also moving the industry in the same direction. Its aim is to make cross-border LPM coverage simpler and more connected for merchants operating across the continent.

Building the right strategy

The practical steps for merchants are laid out in the report, and the outcome is clear: track where your customers are buying from, match that data to the dominant payment method in each market, and build from there.

The demand is there across Europe too — 90% of European consumers have used some form of digital payment in the past year. The question is whether your checkout is ready to meet and accommodate this rampant demand.

Download How Europe likes to pay: navigating emerging cross-border payment methods for country-by-country breakdowns, APM spotlights, and a practical checklist to help you build a checkout strategy that works across every market you serve.