Fraud losses are often measured in hard currency or bottom line figures, but the true, hidden costs are much harder to quantify and recover from for merchants.

Fraud cost UK businesses £1.17 billion in 2024, while the EBA and ECB's joint 2025 report put total fraud across Europe at €4.2 billion for the same year, a 17% increase on the prior year. These figures typically dictate how risk frameworks are established.

However, recent findings from payabl.'s Fraud in Europe: Counting the cost for retailers and shoppers draws attention to what fraud does to a business's reputation, and how it affects the people caught in the middle.

When customers stop trusting you

More than half of businesses (52%) surveyed in the report said fraud had caused reputational damage to their brand. Among larger businesses, that figure rose to two-thirds (67%). Reputational damage is difficult to restore for merchants. Unlike a chargeback or similar type of fraud, it cannot be reversed, and only often appears after a period of time in reports or figures.

The data from consumers highlights this further. One in five (21%) said they permanently stopped shopping with the retailer through which they experienced fraud. A further 20% said they now only shop with larger, more established brands; a direct behavioural shift that harms smaller merchants.

Another 10% of consumers reported spending less online overall following a fraud incident. Holistically, this translates into something beyond a one-off financial loss, and more like a slow bleed or drain over time.

The operational weight merchants are carrying

The reputational consequences faced by merchants can directly impact operational ones. Data shows that 36% of businesses reported a direct loss of income attributable to fraud. Beyond the headline figure, the data reveals more:

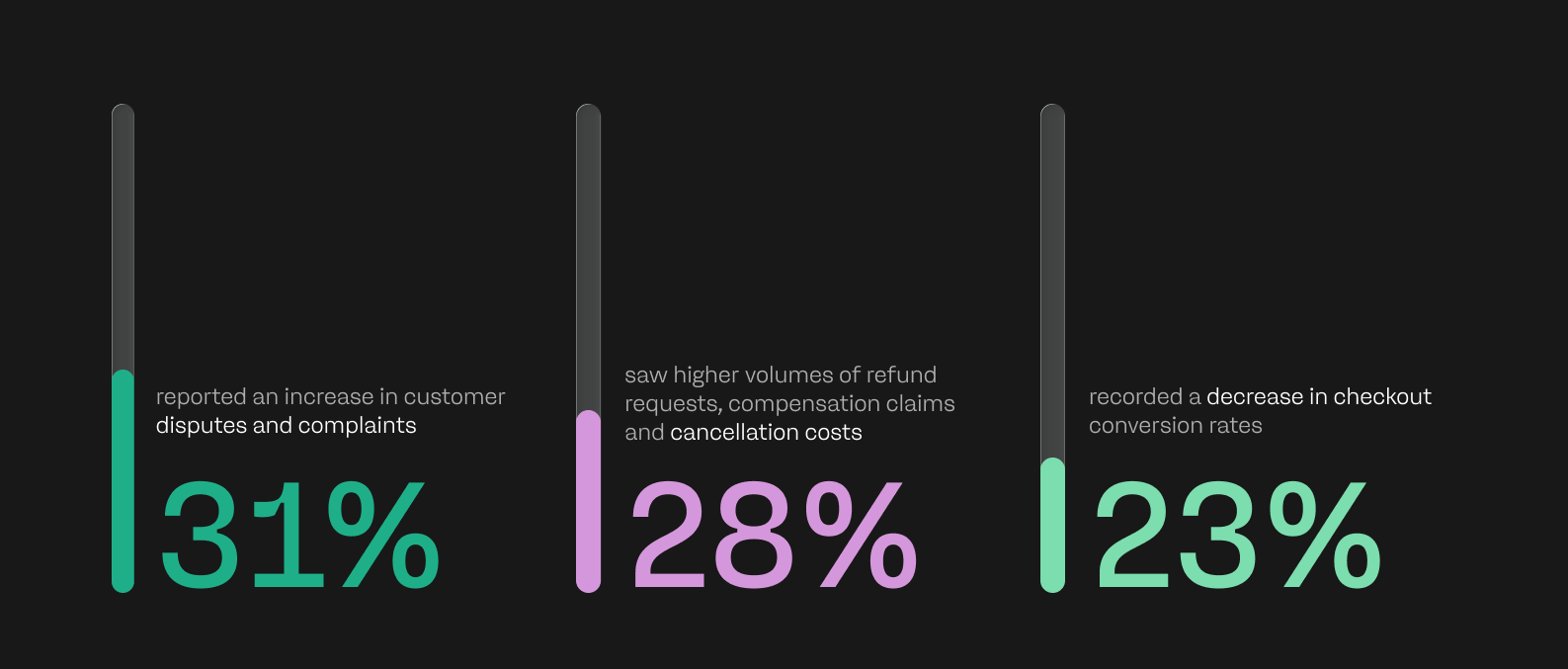

- 31% reported an increase in customer disputes and complaints

- 28% saw higher volumes of refund requests, compensation claims and cancellation costs

- 23% recorded a decrease in checkout conversion rates.

Each of these represents a cost that compounds beyond fraud loss.

The burden on merchant teams is also growing. Three-quarters (74%) of businesses said they are spending more time and resources combatting fraud than they were a year ago, and 84% said they feel personally responsible for preventing it.

This sense of accountability aligns with broader consumer expectations; payabl.'s State of European Checkouts report found that 44% of consumers place the responsibility for fraud prevention on merchants, banks, and payment providers, not on the end user.

This cumulative pressure is ultimately influencing strategic decisions made by merchants. Nearly half (48%) said they have now considered scaling back their operations as a direct result of persistent fraud.

Overall, while fraud is one of multiple contributing factors that can influence a business, payabl.'s data suggests it is actively shaping decisions about whether they can continue to trade and operate at all.

The personal toll on consumers

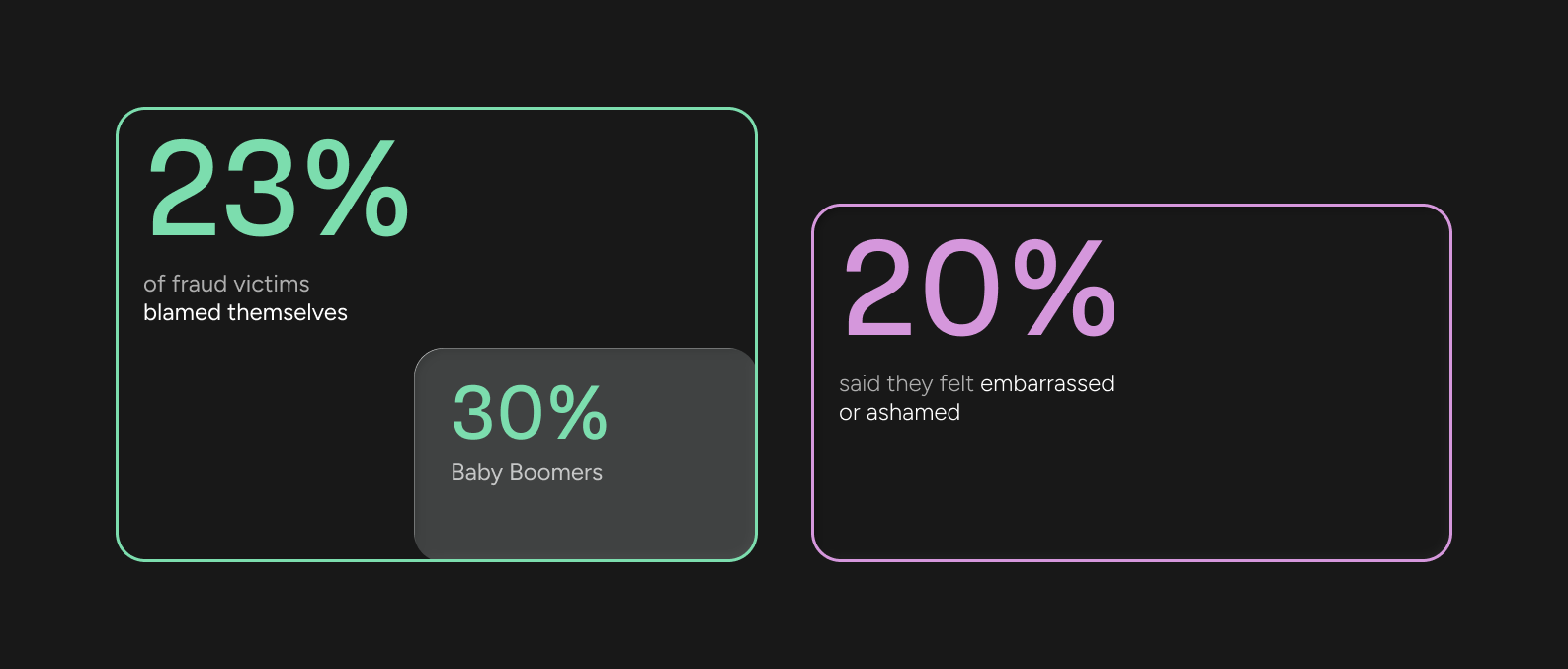

The effects on consumers extend well beyond the financial. Research from the report found that 23% of fraud victims blamed themselves for what happened — a figure that rose to 30% among Baby Boomers — and 20% said they felt embarrassed or ashamed.

This pattern is consistent with wider research. A study from Crest Insights found that the emotional impact of online fraud was frequently worse than the financial loss, even in cases where victims lost large amounts of money.

The victims interviewed reported feelings of shame, isolation, and self-blame, while noting they felt less likely to receive sympathy than victims of more conventional crimes.

The UK government's own research on fraud victim experiences from January 2025 also found that 77% of miscellaneous fraud victims experienced embarrassment, shame, or self-blame.

For payment providers and merchants, this comes with enormous significance. Consumer self-blame can suppress reporting, which skews fraud data. In turn, this can undermine the ability of financial institutions to gain a clear picture of the scale, and identify and respond to emerging threat patterns.

It also reinforces inaction from consumers, who are less likely to contact the merchant, the bank, or the relevant authority after experiencing fraud.

Behavioural change is already underway

41% percent of consumers in the report said they are now more cautious when shopping online, a figure that rises to 46% among women. This heightened awareness introduces an additional layer of friction to the customer journey, and is one that is felt by merchants.

20% of consumers said fraud has prompted them to focus their online shopping on larger, more well-known brands. For smaller and mid-market retailers, this can have disastrous consequences. Now across the market, the feeling of security and brand recognition is becoming a determining factor in where consumers choose to spend.

This shift in behaviour is occurring against a backdrop of rising fraud sophistication, which includes advancements in AI, chargeback-related and romance scams. In 2024, the global ecommerce sector lost $44 billion to fraud, with the total expected to rise and surpass $100 billion by 2029; in a fraud environment where it’s so prevalent, consumers are having to navigate more cautiously to protect themselves.

The opportunity in prevention

The data in the report contains an important finding that could be easily overlooked; 84% of merchants feel responsible for preventing fraud. This sense of ownership and responsibility acts as a source of pressure for merchants, while also serving as motivation to invest proactively in prevention measures.

Consumers who can implicitly trust that a merchant takes security seriously are less likely to abandon their relationship after an occurrence of fraud, and are also less likely to migrate to a larger platform simply on their perception of safety measures.

Overall, 44% percent of consumers believe fraud prevention is the joint responsibility of merchants, banks, and payment providers. This helps merchants, as those who can communicate their position on customer safety and fraud prevention clearly can nurture customer relationships, while proving more resilient to behavioural churn that fraud currently influences.

With this in mind, it’s worth considering that the businesses most exposed to reputational damage are not those experiencing the highest fraud rates, but those without a clear and actionable response to emerging fraud threats.

Download ‘Fraud in Europe: Counting the cost for retailers and shoppers’ to find out how to manage the emotional and reputational costs of fraud.