Nine in ten (87%) merchants acknowledge that preventing fraud effectively is critical to their long-term success, according to payabl.'s fraud in Europe report. The extent of fraud is widely recognised in the industry. Still, only half (50%) of merchants have clear internal policies in place for tackling it. And fewer than half (47%) communicate with their customers about fraud risks or share guidance on staying safe online.

The data shows early momentum, and that merchants are changing their approach. Three-quarters (76%) of merchants are planning to invest more in fraud prevention tools in the year ahead, and 84% say they want better technology to support their efforts.

This investment alone does not signal intent. The merchants making progress are those treating fraud prevention as an operational priority.

Why a reactive approach keeps falling short

Fraud methods are evolving, with AI-assisted scams, identity fraud, and targeted attacks during peak trading periods accelerating. This means merchants who wait for incidents are already a step behind. Reactive fraud management carries layered risk. Chargebacks are processed after money has moved. Disputes take time and resources to resolve. Reputational damage is difficult to reverse

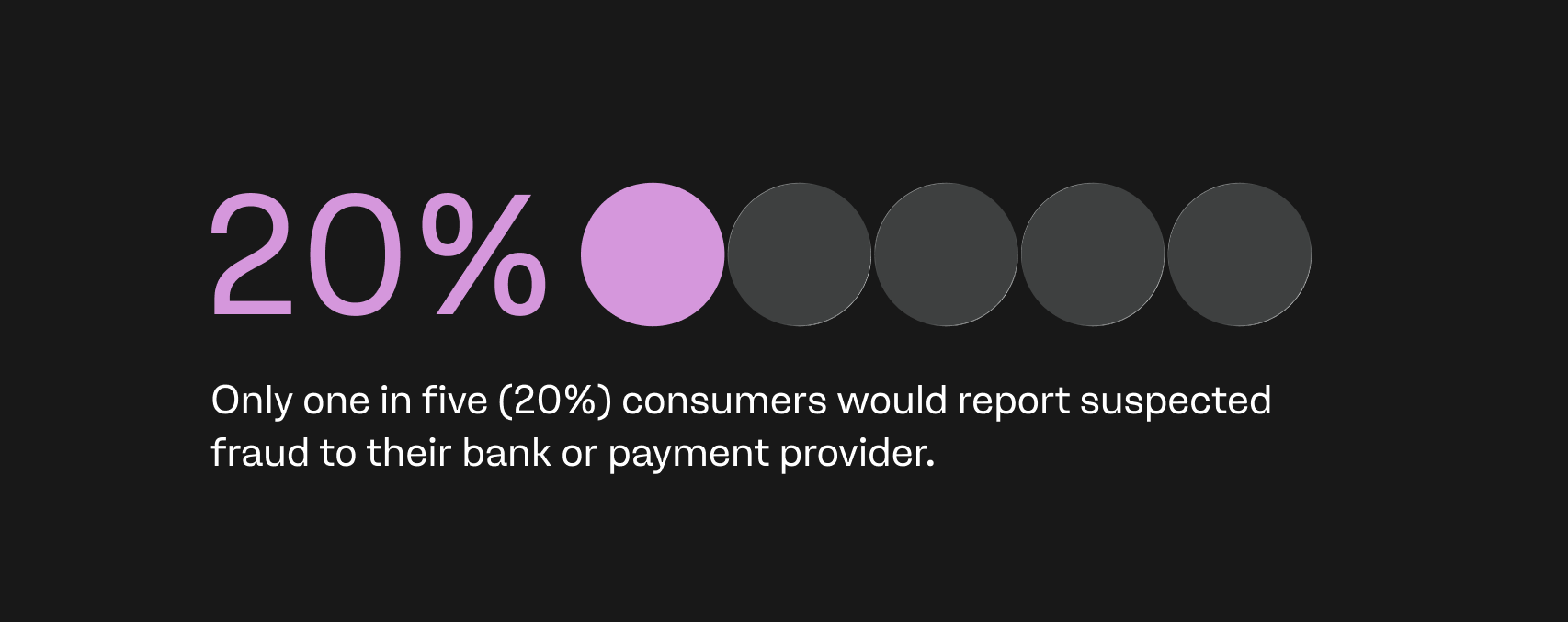

Data from payabl.'s report highlights that only one in five (20%) consumers would report suspected fraud to their bank or payment provider. The trend of underreporting means the true volumes of fraudulent activity faced by a merchant is likely higher than internal data suggests. This blind spot only widens when transaction volumes peak during events like Black Friday or January sales.

The merchants best positioned to address this use real-time transaction monitoring, which flag suspicious activity as it happens rather than in daily or weekly reports. 50% of retailers are already working with payment partners that offer built-in fraud tools. However, this still leaves half the market relying on systems that are not purpose-built for the volume and variety of threats they now face.

The case for Digital IDs, and why implementation matters

Digital identity verification is gaining traction as a practical tool for reducing fraud at the point of purchase. The EU Digital Identity (EUDI) Wallet is currently in development and is expected to be available to all EU citizens and businesses from late 2026. Alongside this, the UK government has announced that Digital IDs will become mandatory for Right to Work checks before the end of the current Parliament.

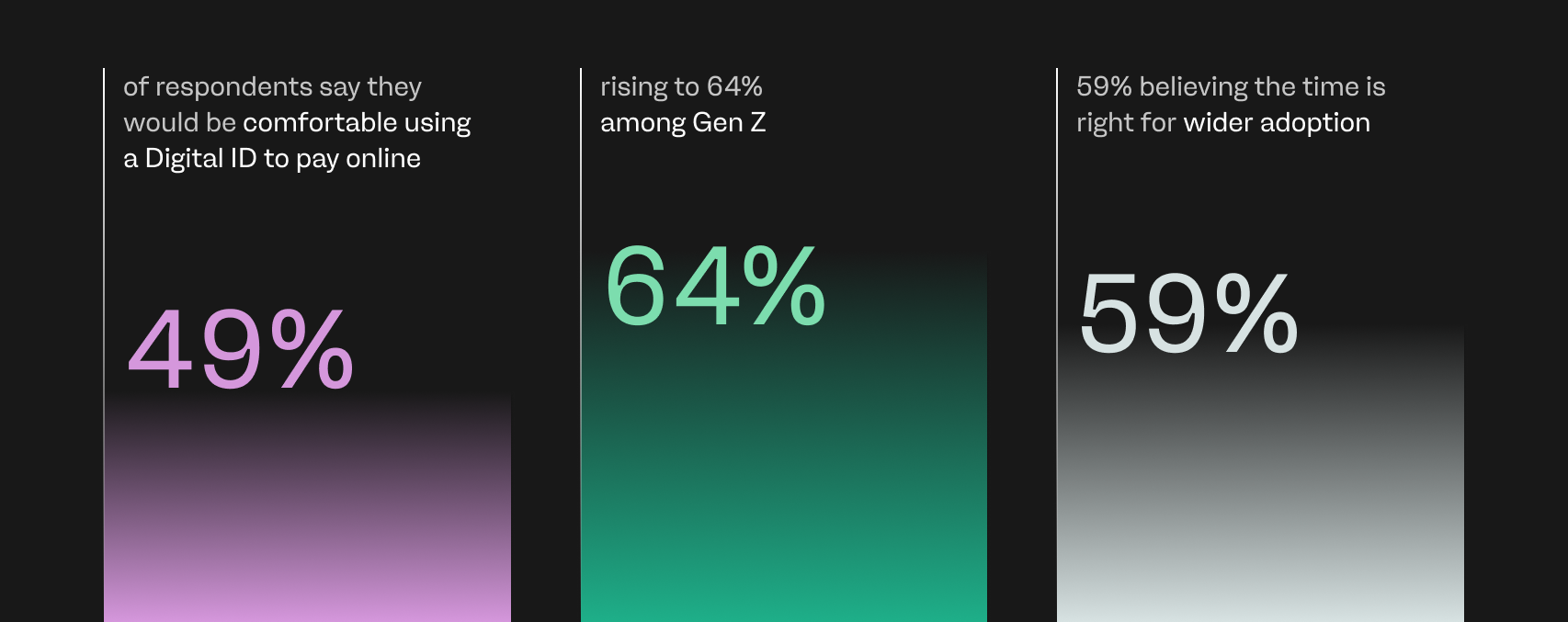

Merchant appetite is clear: 81% say they would incorporate Digital ID payment options if it helped reduce fraud, and the same cohort would adopt them if it improved the checkout experience for customers. Consumer sentiment is supportive too. 49% of respondents say they would be comfortable using a Digital ID to pay online — rising to 64% among Gen Z — with 59% believing the time is right for wider adoption.

The upsides are clear, but caution and reservation around Digital IDs is present. Seventy-nine percent of merchants worry fraudsters will simply find workarounds, and 63% remain sceptical about whether Digital IDs will reduce fraud in practice. Two in five (43%) flag that fraud checks already slow down the checkout experience. 39% cite multiple verification layers as a source of friction. 34% say added friction directly impacts cart abandonment.

The ecosystem needs to pull in the same direction

88% of merchants believe that banks need to do more to intercept fraudulent payments and shut down accounts operated by bad actors. 84% say European governments need to clarify who bears responsibility for fraud losses, while 75% feel that social media platforms are not doing enough to limit fraud that originates or is promoted on their platforms.

payabl.'s Group CEO Ugne Buraciene put it directly in the report: "Reducing fraud will require closer collaboration between merchants and their payment partners. By working in tandem and sharing data, implementing the right compliance measures, and leveraging AI and other emerging technologies, we can balance innovation with consumer confidence and create a safer ecommerce ecosystem."

What consumers actually want at checkout

Security is a deciding factor for most online shoppers. 33% of consumers cite two-factor authentication and extra security controls as the checkout feature most likely to make them complete a purchase with a retailer.

46% say they are more likely to trust retailers who use Digital ID checks. Further findings from payabl.'s The State of European Checkouts report show that most consumers are willing to accept a slightly slower checkout in exchange for stronger fraud protection if the friction is clearly explained.

The implication of this for merchants is practical: visible, well-communicated security measures build consumer confidence. Friction becomes a problem when it appears without clear reason, adds unnecessary steps, or sits outside the checkout flow.

Acting now rather than planning to act later

The data from the fraud in Europe report shows that the merchants who are best placed to protect revenue and customers are those operating proactively. For many, waiting until fraud levels worsen before investing in better tools, or leaving fraud policies undocumented carries financial and reputational risks for merchants.

The full report delivers a detailed breakdown for merchants: the cost of fraud by market, the types of fraud affecting merchants most frequently, the consumer behaviours driving exposure, and the solutions showing promise.

Download fraud in Europe: Counting the cost for retailers and shoppers to understand where your business is most exposed, and what the data says about addressing it.