At payabl., we work with businesses across Europe that operate in multiple markets and manage complex financial infrastructure. A pattern has emerged after working with multi-disciplined merchants: the more their business scales, the harder it becomes to get a clear picture of their finances. For many, reconciliations take longer, liquidity sits idle and reporting is spread across systems that can’t communicate.

Financial fragmentation is a bigger strategic issue than most businesses realise. To help merchants overcome this, we partnered with Juniper Research to find out how widespread the problem actually is and what it's costing businesses.

Fragmentation is a growth constraint

The headline finding from the research is urgent: financial fragmentation is directly impacting profit for merchants. We found that most finance and payments teams are aware that their systems are fragmented. There are too many providers, too many manual processes, and too much time spent on reconciliation.

What the research makes clear is that this creates structural and operational drag, which prevents businesses from moving at speed and providing what the market demands. Fragmented infrastructure slows decision-making and makes scaling into new markets significantly harder than it needs to be.

The numbers are hard to ignore

Fragmentation is easy to dismiss as a low priority problem, but the supporting data reveals the stark reality facing merchants.

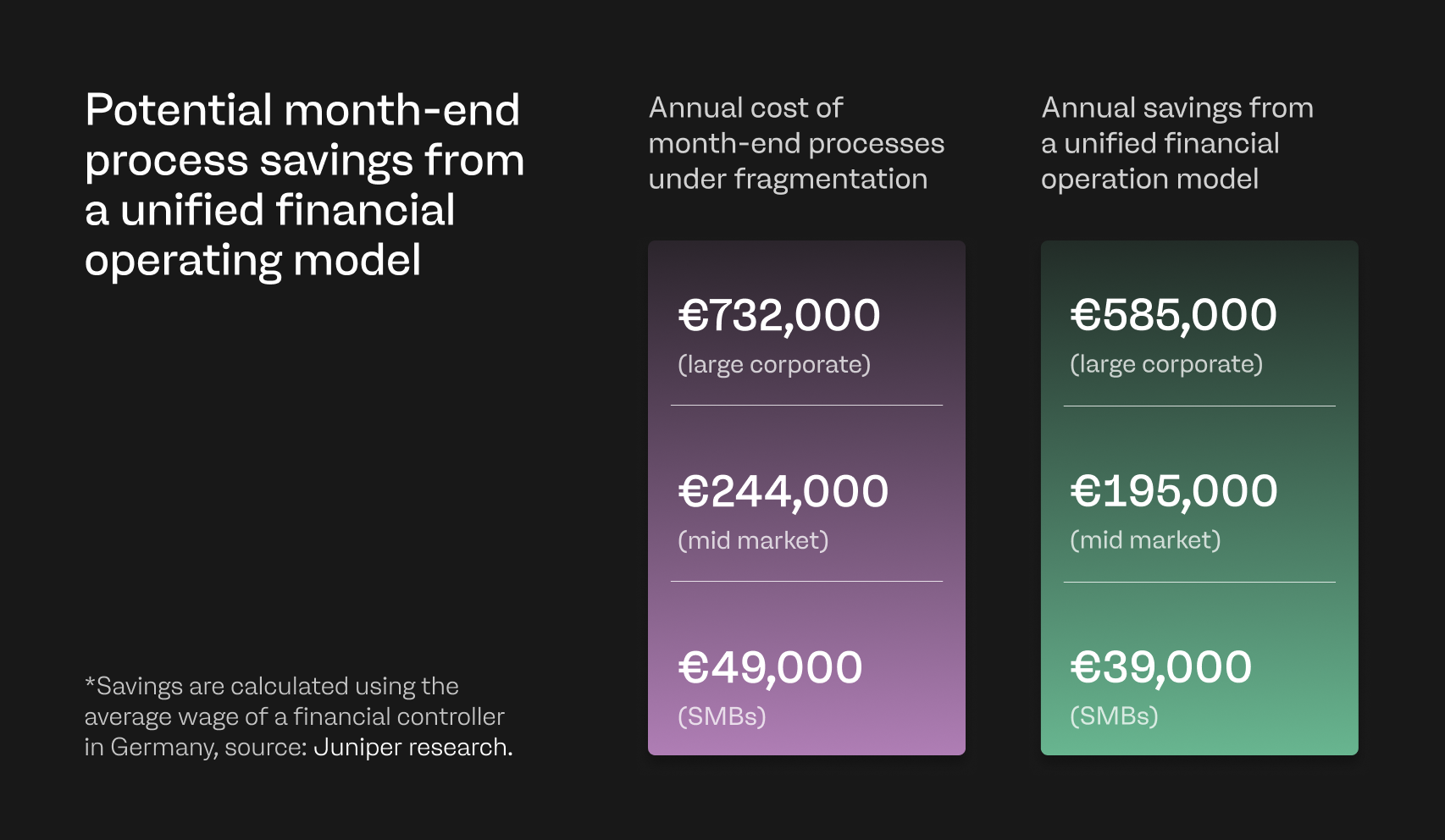

Juniper Research calculated that month-end reconciliation processes in fragmented environments that require heavier manual input can take a financial controller or similar role up to 10 days to complete.

Translated into salary cost using average financial controller wages in Germany, that equates to €49,000 per year for an SMB, €244,000 for a mid-market company, and €732,000 for a large corporation. This only covers the cost of fragmentation from reconciliation, and doesn’t take into account integration overheads, provider fees, or the FX costs that compound with cross-border transactions.

Touching on FX costs, Juniper Research found that the average business faces costs of between 1% and 3% per transaction, and in a multi-provider ecosystem, costs naturally drift toward the higher end of that range. For businesses processing meaningful volume across Europe, ecommerce will be an €11 billion opportunity by 2030, with cross-border accounting for around 38% of the market. This incurs a material impact on operating margin.

Payment complexity is accelerating

Part of what makes fragmentation difficult to solve is that it's a natural by-product of how businesses grow. For merchants, each new market, new provider, and new payment method adds layers, and the research identified several factors making this worse.

In the EU alone, there are almost 1,000 payment institutions authorised under PSD2, according to the European Banking Authority's register as of February 2026. As such, picking the right partner and integrating said partner with a broader financial stack has become a time-costly project in itself.

The payment method side adds further complexity. Cards remain prominent in European checkouts, but are gradually losing market share in favour of APMs which are widely used and embedded across local markets. For example, Swish is used by over 80% of Sweden's population. BLIK processed 2.9 billion transactions in Poland in 2025, reaching 20.7 million users (approximately 55% of the country's population).

Wero and the move toward unified European payments

One of the most significant developments to emerge from the research is the trajectory of Wero. Developed by the European Payments Initiative (EPI) and backed by Europe's largest banks, Wero is built on SEPA Instant rails to consolidate the region's fragmented payment method landscape into a single, sovereign system.

iDEAL | Wero is already live in the Netherlands (previously iDEAL), Germany, Belgium and France, and as of June 2026 had been used by more than 50 million Europeans. Payments clear in under 10 seconds, including cross-border transactions, and the wallet supports P2P, ecommerce and in-person payments. Its expansion across Europe through 2026 and 2027 aims to reduce APM fragmentation which has increased costs and complexity for European merchants.

For PSPs, it presents both obligation and opportunity. Merchants will expect native support as it scales across new markets. In October 2025, payabl. became one of the first licensed members of the EPI and a direct acquirer within Wero. This means PSPs working with payabl. can offer their merchants instant, secure A2A payment acceptance without maintaining additional infrastructure.

The solution requires unification

However, connecting fragmented systems more effectively is not the answer. More integrations create more complexity. The research points to a unified financial operating model as the structural fix: a single platform that consolidates acquiring, banking, FX, payment methods, and reporting into one operating environment.

The savings are substantial. Juniper Research calculated that reducing the reconciliation cycle from 10 days to two days — achievable through a unified model — would save businesses €39,000 per year at SMB level, €195,000 at mid-market, and €585,000 at enterprise scale. But the more significant shift is strategic. A unified model gives businesses the visibility and agility to act on opportunities faster, rather than spending time managing underlying infrastructure.

How payabl. addresses this

payabl.one is built on this principle. Rather than offering isolated products that create their own points of fragmentation, it’s a unified financial operating layer that connects acquiring, 300+ payment methods, multi-currency business accounts, card issuing, FX, reconciliation and reporting in one place.

On the payments side, a single integration gives merchants access to domestic and global card acquiring alongside over 300 payment methods, as well as in-store POS. Merchants can handle acceptance across channels from one place.

Settlement flows directly into multi-currency business accounts with IBANs across more than 60 currencies, so funds are visible and accessible without delays from using separate providers. This integration addresses one of the most consistently reported causes of cashflow visibility problems.

For spend management, virtual business cards close another gap. Teams can issue cards with customisable limits, monitor transactions in real time, and manage everything within the same platform. This reduces fragmentation that comes from using separate tools and banking platforms.

Across the platform, payabl.one consolidates payment data, settlement activity and account reporting into a single dashboard. Teams get a real-time view of financial operations without cross-system aggregation.

For PSPs, payabl.'s infrastructure means their merchant clients can access this full suite through a single relationship, rather than requiring merchants to build out individual connections for each capability.

Get the whitepaper

The whitepaper covers the full scope of findings: how fragmentation affects businesses at different stages of scale, the direct and indirect costs it creates, how payment method complexity is accelerating across Europe, and what a unified financial operating model looks like in practice.