How Visa Click to Pay, tokenisation, and strong UX reduce revenue drain

Checkout optimisation requires balance: move too quickly and you increase exposure to fraud, chargebacks, and failed payments. Add too much security friction and you introduce additional steps, longer completion times, and higher abandonment. In both cases, the outcome is the same, lost revenue at the most critical stage of the customer journey.

Customer expectations are defining ecommerce. Shoppers want the checkout process to feel fast, familiar, and secure. Merchants want higher approval rates, fewer false declines, and better conversion.

This is why one-click payment experiences, including Visa Click to Pay, are becoming a foundation of high-performing checkout strategies. Not simply because they are faster, but because they help merchants address the two biggest challenges in ecommerce payments: friction and trust.

The cost of checkout friction is often underestimated

Many merchants focus conversion improvements on traffic quality, creative, and pricing. However, some of the largest revenue problems occur at checkout, precisely when purchase intent is highest. Conversion tends to drop when a merchant’s checkout introduces:

- Long forms and manual card entry

- Repeated authentication prompts

- Unfamiliar payment flows for first-time shoppers

- Higher error rates from typing card data on mobile

- Guest checkout journeys that feel slower or less trusted than returning checkout

Even a high-performing product page can fail to convert when the final stage introduces hesitation. Modern checkout optimisation is not only UX best practice, it’s a revenue discipline.

One-click payment is more than speed

One-click is often described as a convenience. In practice, the best one-click experiences solve a deeper problem: they reduce customer effort at the moment when intent is most fragile.

A well-designed one-click flow reduces cognitive load and uncertainty. Instead of asking the customer to complete a form, it asks them to confirm a purchase.

High-performing checkouts typically achieve three things: familiarity, safety, and effortlessness.

Click to Pay mirrors the experience of contactless in-store

Visa Click to Pay is designed to reduce manual card entry and streamline ecommerce payments through a standardised checkout experience. It’s designed to mirror the ease of contactless payments in-store.

For merchants, it can be viewed as an express checkout layer for card payments, particularly valuable for:

- Improving guest checkout completion rates

- Increasing first-time buyer confidence

- Optimising mobile conversion

- Reducing payment errors and retries

- Improving approval performance through tokenisation

Importantly, Click to Pay is designed to work without requiring shoppers to download an app, create an account, or remember passwords. That matters because guest checkout performance is often one of the largest drivers of incremental growth.

Tokenisation and approval rates: the conversion-drivers behind the scenes

Checkout improvement is often associated with user experience. However, a significant share of lost revenue happens after the customer has already attempted payment. At that stage, conversion depends on authorisation.

Approval rates are influenced by more than a customer’s available funds. They are affected by risk signals, fraud controls, data quality, and the overall confidence a transaction creates for issuers.

What does tokenisation change at the checkout?

In traditional ecommerce flows, the transaction relies on manual PAN entry. PAN data is static and more vulnerable to exposure, misuse, and fraud attempts. It also provides fewer modern risk signals. Tokenisation is a way to change this model.

Rather than transmitting raw card data, a transaction uses network tokens. These tokens are designed to improve security and strengthen transaction integrity.

Visa’s Click to Pay is secured by Visa Network Tokens, supporting both fraud reduction and improved payment outcomes.

How do tokenised flows boost authorisation rates?

When payment signals improve, issuers are more likely to approve legitimate transactions. This is particularly relevant for false declines, where valid payments are rejected due to overly cautious risk models. Click to Pay is positioned as delivering up to 5% higher authorisation rates1 compared to manual PAN entry.

For merchants, the practical takeaway is straightforward: A faster checkout matters, but a more successful authorisation decision matters even more.

Faster checkout protects the ‘decision moment’

Ecommerce has a narrow window where intent is highest. Checkout is that moment. Each additional second introduces time for the consumer to reconsider:

- “Do I really need this?”

- “Is this site trustworthy?”

- “Why is this taking so long?”

- “I will come back later.”

Long or unfamiliar checkouts do not only create friction. They create doubt. Click to Pay has been positioned as up to 20 seconds faster2 than manual card entry, which can be meaningful in high-abandonment checkout environments, especially on mobile.

Fraud reduction also supports conversion performance

Fraud is typically discussed as a cost problem. It is also a conversion problem.

When fraud rises, merchants often respond by tightening risk controls. That reduces losses, but it can also increase declines, introduce step-up friction, and reduce approval rates for legitimate customers.

Tokenised one-click checkouts help improve that balance by:

- Reducing exposure of sensitive card data

- Strengthening transaction trust signals

- Lowering fraud susceptibility

- Reducing the operational need for aggressive risk rules

Click to Pay is positioned as delivering up to 80% less fraud reported3, supported by tokenisation and passkeys.

For many merchants, the benefit is not only fewer fraud incidents, but a checkout environment that can stay fast while remaining secure.

Practical checkout optimisation tips merchants can apply

Click to Pay and other one-click payments can play a meaningful role in conversion improvement, but strong checkout performance typically results from multiple optimisations working together.

Here are several practical changes that consistently drive improvement:

Design guest checkout as your primary checkout path

Many merchants build the best journey for returning shoppers, then accept higher friction for guests.

In practice, guest checkout is where growth is often won or lost. Adding one-click checkout options directly into the guest journey reduces friction at the point where trust is not yet established.

Reduce manual input wherever possible

Manual entry increases:

- Errors and failed payment attempts

- Retries and abandonment

- Customer support issues

- Perceived effort, particularly on mobile

Removing unnecessary form completion is one of the most reliable ways to improve checkout completion rate.

Reinforce trust at the payment moment

Trust signals matter most at the final step.

Common drivers include:

- Familiar payment iconography and options

- Security reassurance that is clear and unobtrusive

- Clean, standardised payment interface

- Minimal ‘surprise’ steps at the end of checkout

One-click payments reduce the need to enter sensitive details into unfamiliar websites, supported by trusted issuer and network protections.

Optimise for approval rates, not only visual design

Merchants should treat checkout performance as a combination of UX and payments acceptance.

This includes: tokenisation where available, effective retry logic for soft declines, strong routing and risk design that avoids false positives, and clear monitoring of approval rate changes post-launch.

Use authentication approaches that minimise friction

Security is essential, but it should not feel like a disruption.

Modern approaches aim to validate identity through device trust and biometrics. Click to Pay uses OTP authentication as part of enabling faster, more secure checkout authentication.

How payabl. supports adoption and performance

For many merchants, the challenge is not identifying improvements. It is implementing them quickly and safely, without rebuilding checkout flows or creating additional compliance burden.

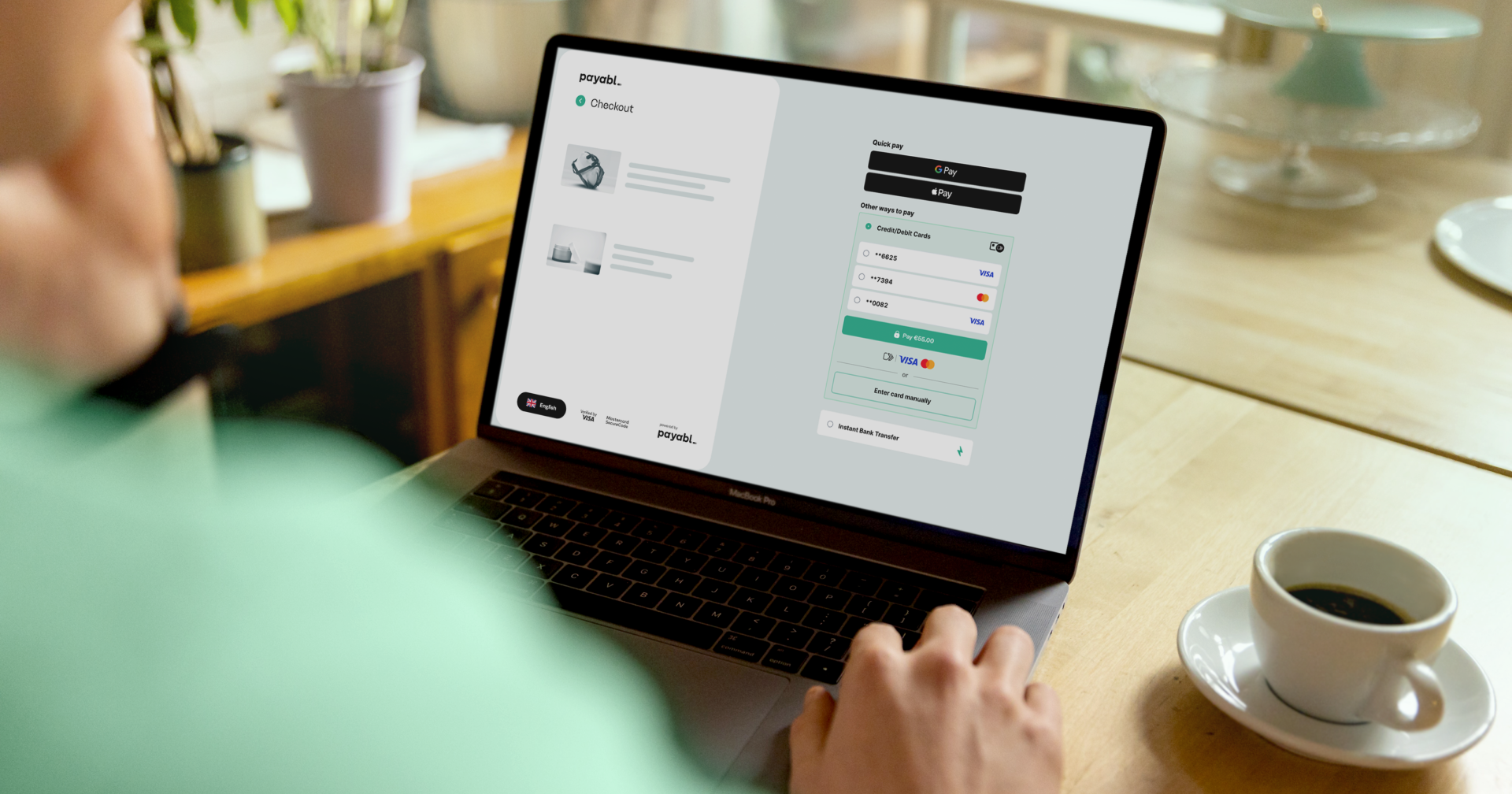

payabl. enables Click to Pay through a Hosted Payment Page approach, helping merchants activate one-click checkout with reduced complexity while maintaining control and consistency across the payment experience.

How to get started with Click to Pay

For merchants looking to reduce checkout friction and improve conversion outcomes, Click to Pay is a practical optimisation, particularly for guest checkout and mobile-first audiences.

A structured rollout typically includes:

- Identifying the checkout stages with the highest drop-off

- Establishing baseline conversion and approval rate metrics

- Enabling Click to Pay via payabl. checkout

- Monitoring conversion uplift, approval changes, and fraud trends post-launch

To get started with Click to Pay, speak to your payabl. account manager or contact our payments experts to discuss ways to improve checkout performance.

1. VisaNet Data, GBI Monthly Authorisation Report, May 2022 // 2. Click to Pay Visa pilot data, 2023. // 3. Global Risk Team, Visa Net, CTP Fraud Rates, June 23–May 24, compared to PAN-based transactions online

Case studies, comparisons, statistics, research, and recommendations are provided “AS IS” for informational purposes only and must not be relied upon as operational, marketing, legal, technical, tax, financial, or other professional advice. payabl. makes no representations or warranties, express or implied, as to the completeness, accuracy, or adequacy of the information contained above and assumes no liability or responsibility for any loss or damage arising from reliance on such information. The information contained herein does not constitute investment or legal advice. Readers should seek advice from qualified professional advisers where appropriate.