Most merchants don't set out to build fragmented financial infrastructure. The process happens gradually. First comes a PSP integration. This is followed by an additional business account partner and finally a solution to solve a specific problem in a specific market. Over time, this creates disconnected systems that create friction across business operations.

According to new information commissioned by Juniper Research, this fragmentation is becoming a direct constraint on growth, and the problem runs deep. As merchants expand, their financial infrastructure often fails to keep pace. Fragmentation delays reporting, forces manual reconciliation, and traps liquidity. As a consequence, data sits siloed across platforms that can’t interact with each other.

The scale of the burden

The cost of fragmentation to merchants is quantifiable. For example, Juniper Research estimates that month-end reconciliation processes take a financial controller up to 10 days. At current levels, that translates to an annual cost of approximately €49,000 for an SMB, €244,000 for a mid-sized merchant, and €732,000 for a large corporation.

That figure covers reconciliation alone before FX costs. The data from Juniper Research also indicates the average merchant faces FX costs of between 1% and 3% on transactions. The savings of businesses using a unified financial operating model are revealed in the whitepaper. Ultimately, the outcome is that the more complex the provider stack, the higher the costs.

Where the fragmentation is coming from

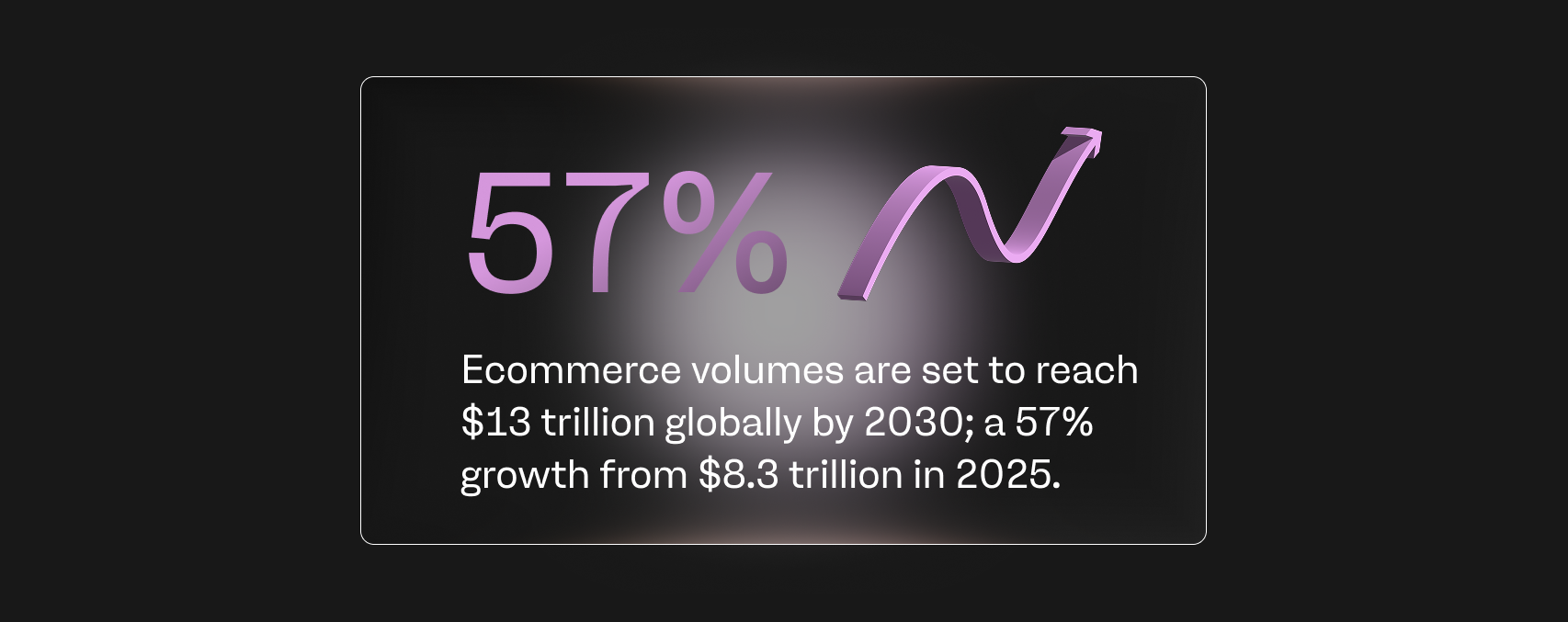

Several structural trends are driving this shift. Ecommerce volumes are set to reach $13 trillion globally by 2030 according to Juniper Research's eCommerce Payments Market report; a 57% growth from $8.3 trillion in 2025. This means every new market a merchant enters introduces new business account relationships, new regulatory requirements, and new payment method preferences.

The payment method side is particularly pronounced in Europe. BLIK processed 2.9 billion transactions in Poland in 2025, reaching 20.7 million users. iDEAL | Wero accounts for approximately three-quarters of online payment volume in the Netherlands. For any merchant trying to serve consumers across European markets, supporting these methods individually creates enormous operational overhead.

Meanwhile, the PSP market itself is scaling rapidly. The European Banking Authority's payments institutions register recorded almost 1,000 authorised payment institutions under PSD2 in the EU alone as of February 2026. Subsequently, choosing the right partner and integrating that partner within a merchant’s wider financial stack introduces additional workload.

The compounding effect on different merchant types

The nature of fragmentation changes depending on the size of the merchant, but core problems exist for all of them.

For SMBs, limited resources mean that manual reconciliation consumes a disproportionate share of finance team capacity. The absence of connected cross-border tools means absorbing traditional friction costs such as slow settlements, unclear FX rates and limited payment method access.

Mid-market merchants often have more systems in place, but this also causes integration strain. While APIs have lowered the barrier to connecting systems, these connections still require development work and ongoing maintenance, pulling engineering resources away from product launches.

For enterprises, the challenge compounds further. Multi-entity operating structures often silo liquidity at entity levels, limiting flexibility and freedom of treasury teams when deploying capital across the group.

Visibility as the core problem

Across all these merchant types, the underlying issue stems from reduced visibility. Often, fragmented data environments produce inconsistent reporting and limit access to real-time insights. Merchants lose sight of the full picture, and can’t aggregate information from multiple sources. This lack of visibility creates delayed decisions and missed opportunities for merchants.

Plus, data fragmentation heightens compliance risks for merchants. With multiple providers and multiple systems in place, audit trails become more complex, increasing the likelihood of errors during manual reconciliation.

What merchants need to consider now

Merchants expect speed, faster settlement and real-time financial data. However, payment methods are multiplying, and fragmentation is increasing as merchants need more and more to compete with today’s changing markets.

Financial fragmentation is no longer just an operational inconvenience. It is becoming a direct constraint on growth. As businesses expand across markets, entities and payment ecosystems, disconnected financial infrastructure slows decision-making, reduces visibility and makes scale harder to manage.

The answer is not another point solution layered on top of existing complexity. It is a unified approach to how money flows, one that connects acquiring, accounts, payments and financial operations into a single, coherent flow.

This is the principle at the heart of what we do at payabl. We exist to make money flow: across borders, between systems and through every layer of a business's financial stack. Because when money flows without friction, businesses don't just run more efficiently. They see further, move faster and compete more effectively.

According to the research by Juniper, the companies that unify their financial infrastructure now won't simply keep pace with complexity. They will turn it into a competitive advantage.

The full report will be available to download soon.