A digital wallet is a software application that securely stores a customer’s payment credentials, such as credit cards, debit cards, and bank account details, so they can pay without entering card numbers by hand. In practice, a digital wallet turns a phone, laptop, or wearable into a payment instrument. For a merchant, that matters because a shopper who can pay in one tap is far less likely to abandon the cart.

Digital wallets are now mainstream in the UK: more than half of UK adults already use a mobile wallet to pay, and wallets account for a growing share of online checkouts every year. For a business, this means a checkout without wallet payments is quietly leaking revenue.

Think of a digital wallet as a hotel concierge for money. Instead of the guest fumbling for keys, directions, and cash at every turn, the concierge already holds everything and hands over exactly what is needed, instantly and securely. Your customer gets the same feeling at checkout: no friction, no fumbling, just a smooth tap.

Designed for UK merchants, this guide breaks down how digital wallets function, their different types, and their overall safety. It also details the advantages, disadvantages, processing mechanisms, and pricing of wallet payments, alongside actionable steps to begin accepting them across all channels.

How does a digital wallet work?

A digital wallet works by storing tokenised payment details and transmitting them securely when a customer pays. The card number is replaced with a unique token, so the real details are never exposed to the merchant or intercepted in transit. Payment is then authorised using a fingerprint, face scan, or PIN.

Here is the flow in four steps a merchant should know:

- The customer adds a card to the wallet, which is converted into a secure token by the card network.

- At checkout, online or in store, they select the wallet as the payment method.

- They confirm with biometrics or a PIN, so the transaction is strongly authenticated.

- The token is sent to the payment provider, the issuing bank approves it, and funds settle to the merchant.

The underlying technologies vary by context. In store, wallets use Near Field Communication (NFC) for contactless taps, while some devices also support Magnetic Secure Transmission (MST) or QR codes. Online, the wallet passes the token to the payment gateway. Because wallet transactions are tokenised and biometrically authenticated, they usually satisfy Strong Customer Authentication (SCA) under PSD2 with less friction, which is one reason wallet payments tend to lift approval rates.

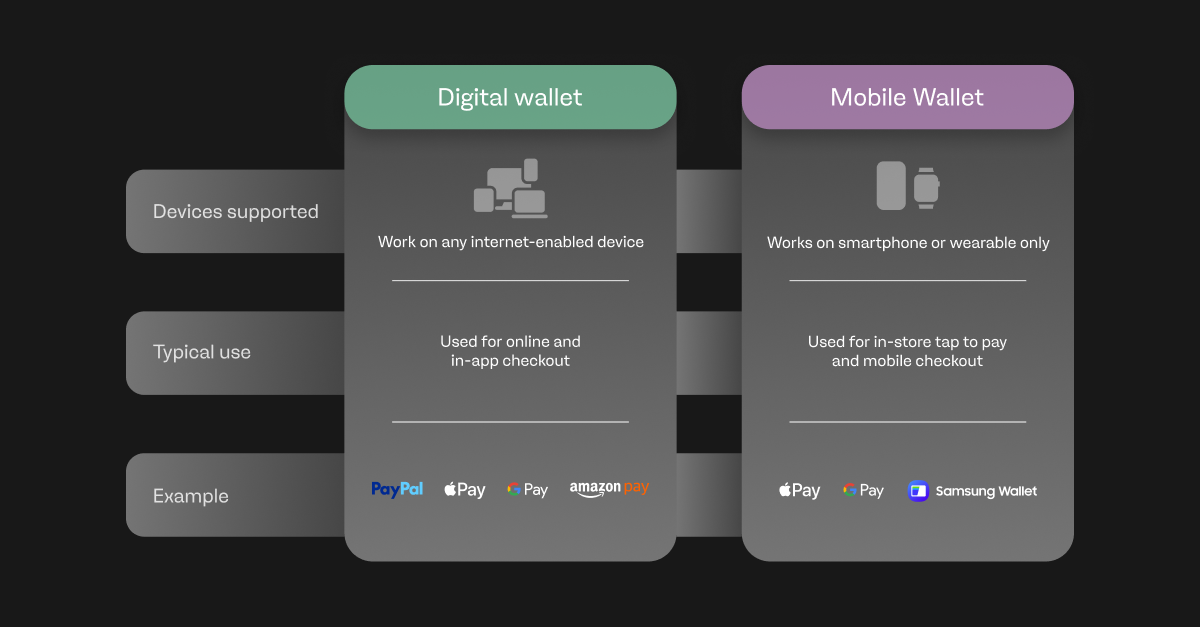

Digital wallet vs mobile wallet: what is the difference?

The main difference is scope: a digital wallet is any software that stores payment details and can be used across devices, while a mobile wallet is a digital wallet built specifically for a smartphone or wearable. Every mobile wallet is a digital wallet, but not every digital wallet is a mobile wallet. An electronic wallet, or e-wallet, is simply another name for the same concept.

For a merchant, the label matters less than the coverage. What you want is a payment setup that accepts wallet payments wherever your customer is: on the website, in the app, and at the physical counter.

| Aspect | Digital wallet | Mobile wallet |

| Devices | Any internet-enabled device (desktop, laptop, phone, wearable) | Smartphone or wearable only |

| Typical use | Online checkout and in-app payments | In-store tap to pay and mobile checkout |

| Examples | PayPal, Apple Pay, Google Pay, Amazon Pay | Apple Pay, Google Pay, Samsung Wallet |

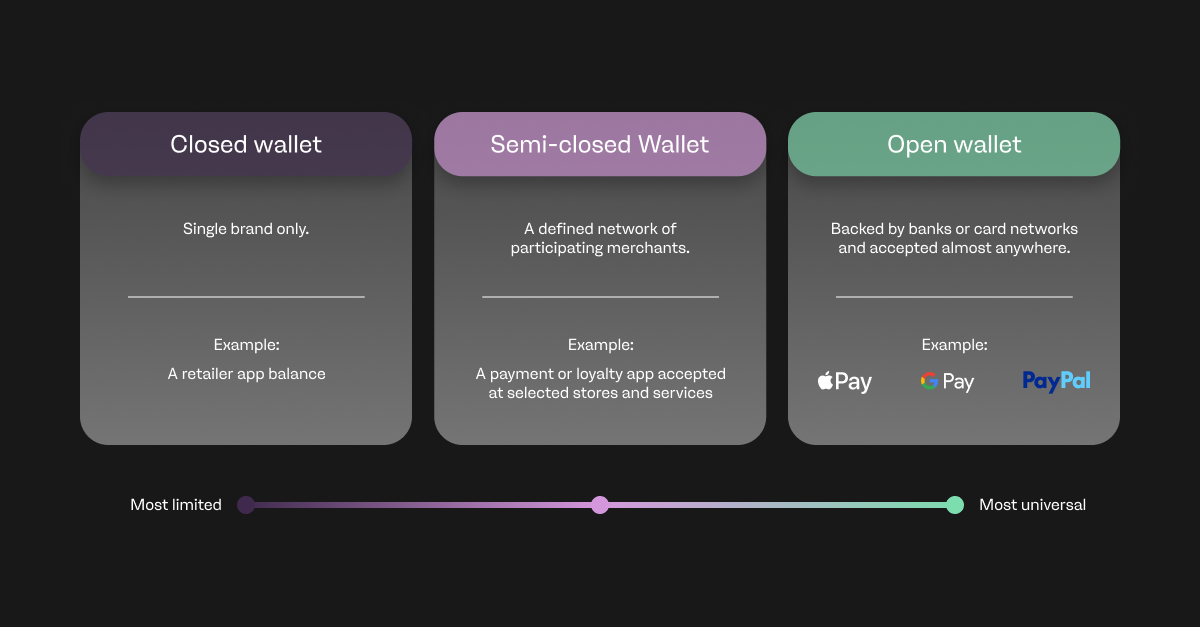

Types of digital wallets

There are three main types of digital wallets a merchant will encounter:

- Closed wallets: issued by a single brand and usable only with that brand, for example a retailer’s own app balance.

- Semi-closed wallets: usable across a defined network of participating merchants.

- Open wallets: backed by banks or card networks and accepted almost anywhere, such as Apple Pay, Google Pay, and PayPal.

Open wallets carry the widest reach, so they are usually the priority when a merchant wants to accept digital wallet payments across UK and international markets.

Popular digital wallet examples

The wallets a UK merchant should recognise are Apple Pay, Google Pay, Samsung Wallet, and PayPal. Offering the wallets your customers already use is one of the fastest ways to raise conversion and approval rates.

| Wallet | Devices supported | Key strength for merchants |

| Apple Pay | iOS devices only | Strong biometric security and high checkout completion on iPhone traffic |

| Google Pay | Android devices | Wide Android reach and stored loyalty cards |

| Samsung Wallet | Samsung devices | NFC and MST support, works with more terminals |

| PayPal | Any device | Trusted online brand, international coverage, buyer familiarity |

How are digital wallet payments processed?

A digital wallet payment is processed much like a card payment, but with tokenisation layered on top for security. When a customer confirms payment, the wallet sends the token, not the real card number, to the payment gateway. The gateway routes it to the issuing bank for authentication and approval in real time. Once authorised, the funds are captured and confirmation is sent to both the customer and the merchant.

Two practical points matter to a finance leader:

- Settlement times: wallet transactions typically settle within one to three business days, depending on the payment provider, the same window as standard card payments.

- Fees: wallet processing fees are generally comparable to card fees, because the wallet rides on the existing card rails rather than adding a separate scheme cost.

Are digital wallets safe?

Yes, digital wallets are generally safer than physical cards because they use tokenisation, encryption, and biometric authentication. The merchant never sees or stores the raw card number, which shrinks the surface area for fraud and reduces PCI DSS scope. If a phone is lost, the payment credentials are locked behind a fingerprint or face scan, not sitting in plain view like a card in a stolen wallet.

For UK merchants there is a compliance upside too. Because wallet payments arrive strongly authenticated, they help satisfy the SCA requirements introduced under PSD2, reducing declined transactions caused by authentication friction. That said, wallets are not risk-free: their smoothness can attract friendly fraud and chargebacks, so a merchant still needs solid fraud tooling and clear refund policies.

Benefits of digital wallets for business

For merchants, the benefits of digital wallets go straight to the metrics that finance leaders track:

- Higher conversion: one-tap checkout removes the biggest cause of abandonment, which is manual card entry.

- Better approval rates: tokenised, biometrically authenticated payments are approved more often and pass SCA cleanly.

- Lower fraud and chargeback exposure: tokenisation keeps raw card data out of your systems.

- Faster mobile checkout: essential when most UK traffic is on a phone.

- Global reach: supporting the right local and international wallets unlocks new markets without building new checkouts.

Why digital wallet payments matter for ecommerce and subscriptions

Digital wallets have moved from a nice-to-have to a default expectation. In the UK, mobile wallet adoption is already past the halfway mark among adults, and wallets account for a rising share of global online purchases, so a checkout without wallet payments is quietly losing sales to competitors who offer them.

For a subscription or SaaS business, there is a second win: wallets store credentials on file and update them automatically when a card is reissued. That reduces involuntary churn from expired cards, protecting the recurring revenue a CFO watches most closely.

How to start accepting digital wallet payments

A merchant accepts digital wallet payments by working with a payment provider that supports them across every channel. The setup is straightforward:

- Choose a payment provider that supports Apple Pay, Google Pay, and other wallets your customers use.

- Make sure in-store terminals are NFC-enabled for contactless taps, or use Tap to Pay on a compatible phone.

- Integrate wallet payments into your online checkout through a secure payment gateway.

- Enable the wallet buttons prominently at checkout so customers see the fast option first.

- Monitor approval rates and conversion to confirm the uplift, then expand to more local wallets by market.

The future of digital wallets in the UK

Wallet adoption in the UK is set to keep climbing, driven by contactless habits, wearables, and new entrants. A notable development is GOV.UK Wallet, the UK government’s digital wallet for official documents and identity, which signals that the wallet is becoming the default place people keep not just payment cards but credentials of every kind. For merchants, the direction of travel is clear: the checkout that meets customers inside their wallet will win the sale.

How payabl. helps UK merchants accept digital wallets

payabl. supports the full omnichannel payment journey, so a merchant can accept digital wallet payments online at checkout, in store through POS, and on the move with Tap to Pay. That means one partner across every place a customer chooses to pay, whether they tap a phone at the counter or breeze through an online cart with Apple Pay or Google Pay.

To explore accepting wallet payments across your channels, get in touch through the payabl. contact form.

Digital wallets are now the default way UK merchants win at checkout

A digital wallet is far more than a convenient way for customers to pay; it is a growth lever for the merchant. By storing tokenised credentials and confirming payment with a fingerprint or face scan, digital wallets remove the friction that kills conversion, raise approval rates, ease SCA compliance, cut fraud exposure, and keep subscription revenue flowing when cards expire.

In a market where most UK adults already pay by wallet, offering wallet payments across online, POS, and Tap to pay is no longer optional; it is how you keep pace with customer expectations and outperform competitors who still force manual card entry. Meet your customers inside the wallet they already trust, and a simple checkout becomes a durable competitive advantage. Digital wallets are now the default way UK merchants win at checkout.

Frequently asked questions

What is a digital wallet in simple terms?

A digital wallet is an app that securely stores your payment cards and lets you pay with a tap or click instead of typing card details. For a merchant, it is a faster, safer checkout that reduces cart abandonment.

How does a digital wallet work?

A digital wallet stores your card as a secure token and authorises payment using biometrics or a PIN. The token, not your real card number, is sent to the payment provider, which requests approval from the issuing bank and settles funds to the merchant.

What is the difference between a digital wallet and a mobile wallet?

A digital wallet is any software that stores payment details across devices, while a mobile wallet is a digital wallet made specifically for a smartphone or wearable. Every mobile wallet is a digital wallet, but not the other way around.

Are digital wallets safe for merchants and customers?

Yes. Digital wallets use tokenisation, encryption, and biometric authentication, so the merchant never handles raw card data. This lowers fraud risk and reduces PCI DSS scope, though merchants should still use fraud tools to manage chargebacks.

What are the disadvantages of a digital wallet?

Wallets depend on a charged, connected device, no single wallet covers every customer, and their smooth checkout can attract friendly fraud. Merchants also need both NFC terminals and an online gateway configured to accept each wallet.

What are examples of digital wallets?

Common examples in the UK include Apple Pay, Google Pay, Samsung Wallet, and PayPal. Offering the wallets your customers already use helps increase conversion and approval rates.

How can a UK merchant accept digital wallet payments?

A merchant accepts digital wallet payments by working with a provider that supports them across channels. payabl. enables wallet payments online, at POS, and via Tap to Pay through a single omnichannel setup.