Switzerland operates one of Western Europe's most self-contained, region-specific payment markets. Consumer preferences skew heavily toward domestic solutions in Switzerland, with TWINT, the leading Swiss mobile payment app, sitting comfortably as the dominant choice.

TWINT was launched in 2017, backed by Switzerland's major banks and PostFinance. By 2025, it had surpassed 6 million active users (equivalent to roughly two in every three Swiss people), with 99% of the Swiss population over the age of 16 recognising the brand.

How TWINT works at checkout

Consumers use TWINT via a smartphone app linked to their bank account or a prepaid balance. When shopping online, the consumer selects TWINT at checkout, scans a QR code displayed on the payment page, and confirms the transaction within the app. In-store payment works via QR code or Bluetooth connection to a POS terminal.

TWINT works like most modern payment methods; no card details are exchanged, no separate account registration is required and the merchant receives payment immediately upon confirmation.

TWINT also handles the authentication process entirely within the consumer's banking environment without any redirects to third-party platforms. For merchants, this means a checkout experience that meets Swiss consumers where preferred payment habits sit.

TWINT’s scale across Switzerland

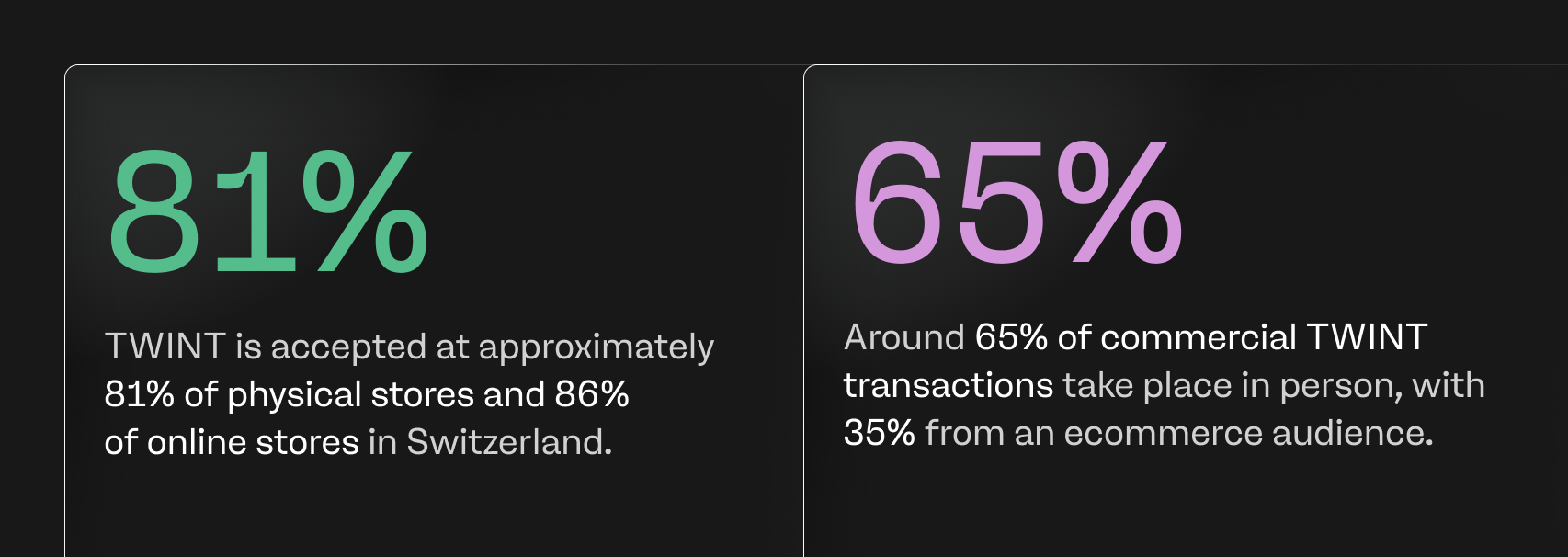

TWINT’s coverage across Switzerland is widespread. It’s accepted at approximately 81% of physical stores and 86% of online stores in Switzerland. Around 65% of commercial TWINT transactions take place in person, with 35% from an ecommerce audience. In 2025, TWINT processed over 901 million transactions, with the app covering a wide range of transaction scenarios beyond standard retail checkout.

This includes peer-to-peer transfers, public transport and mobility payments (77 million transactions in 2024), loyalty card integration with major Swiss retailers including Coop and Migros and charitable donations. A single integration gives merchants access to these use cases without additional development or overheads required.

TWINT has also introduced an Express Checkout feature for ecommerce, allowing consumers to pre-save delivery details in the app and share them at checkout — eliminating manual data entry and reducing friction at the point of conversion. The feature is currently available for merchants using Magento, Shopware, and WooCommerce.

TWINT's positioning within the Swiss market

TWINT accounts for approximately 64% of all mobile payment transactions in Switzerland, according to the ZHAW and HSG Swiss Payment Monitor. That reach extends across demographics: TWINT users range in age from 12 to over 100, covering every generation.

The Swiss National Bank's 2024 Payment Methods Survey confirmed TWINT as the most prevalent mobile payment app in Switzerland, with substantial market share alongside PostFinance's debit card. For context, the Swiss ecommerce market is one of the highest in Europe by per-capita online spend. Paired with the 86% online store acceptance rate, a TWINT integration carries real commercial weight for merchants considering Swiss expansion.

Advantages for merchants integrating TWINT

For merchants, offering TWINT in a Swiss checkout creates an opportunity to improve conversion rates. Swiss consumers encounter TWINT daily, and it exists well beyond a retail perspective for many consumers. As such, merchants who present it prominently in their checkout alongside major card options align with the default expectation of Swiss consumers.

Operationally, a TWINT integration covers the entire payment lifecycle for merchants. TWINT's Business Portal provides real-time transaction monitoring, push notifications for incoming payments, and multi-user role management – ideal for those managing multiple locations or sales channels.

How payabl. simplifies TWINT integration

Through payabl.'s checkout, merchants can offer TWINT alongside 300+ payment methods via a single integration, ensuring localised checkouts for the Swiss market without needing additional technical infrastructure. Merchants don’t require a separate Swiss acquiring relationship or local checkout setup to start with.

For merchants already active in European markets and weighing Swiss expansion or building a multi-market payments strategy, this keeps technical overheads low while matching local consumer expectations.