Failed payments create revenue drag because they interrupt cash flow, trigger avoidable support work, and can turn a short-term payment failure into churn. In the UK, ONS real-time indicators show the seasonally adjusted Direct Debit failure rate rose 11% year on year in December 2025 (and up 1% month on month), which signals that payment failure pressure can move meaningfully even in mature rails.

At the same time, the European Central Bank reports that the euro area processed 77.7 billion non-cash payment transactions worth €116.0 trillion in the first half of 2025, so even small reductions in failed payments can protect real revenue at scale.

What does a failed payment mean?

A failed payment means the payer tried to complete a charge, but the funds didn’t move and the transaction didn't settle. A decline can happen when a bank rejects the request, when authentication doesn't complete, or when the network returns an error. Data issues can also cause failed transactions when the details don't match what the issuer expects.

Essentially, payments fail when the merchant doesn’t receive funds for that attempt. A common cause is a problem with the payment method, such as expired credentials, insufficient funds, or a bank rule that blocks the transaction.

Common payment failure reasons

A failed payment can come from the customer, the bank, or the merchant’s own setup. Each route creates different payment issues and needs a different fix.

A good first step is to classify every failed payment by the point of failure. That approach makes each payment attempt easier to diagnose. It also helps teams reduce repeat failures over time.

Customer-side reasons

Customer-side causes often happen before the bank can approve the transaction. The customer’s payment fails when the account cannot support the charge or the details are wrong. Some failures come from insufficient funds in a bank account. Other failures come from an expired card or incorrect entry of payment data. At times, failures come from fraud prevention checks that the customer can't see. Finally, some failures come from simple user errors during the payment attempt.

Here are the most common customer-side causes and how they differ.

Customer-side reason | What it looks like | Typical signals to log | Best first fix |

| Insufficient funds | The charge is declined because the balance is too low. | Decline response that indicates insufficient funds. | Retry at a better time and offer an alternative method. |

| Expired card | The stored credential is out of date and the charge is rejected. | Expiry date validation failure or issuer decline tied to an expired card. | Prompt an update and use card updater support where available. |

| Incorrect card data | The payer enters details that do not match the card record. | CVV mismatch or number format validation errors. | Improve field guidance and reduce friction in form entry. |

| Mismatched billing address | Address checks fail because the details do not align. | AVS mismatch or a mismatched billing address indicator. | Ask for a corrected address and prefill where possible. |

| Fraud detection triggers | Risk checks block the charge based on behaviour or context. | Elevated risk score and rule hit from fraud prevention. | Step up verification and tune rules to reduce false positives. |

| Other user errors | The user abandons authentication or closes the flow. | Drop-off events and incomplete authentication states. | Simplify the flow and improve messaging at each step. |

Bank & issuer-related reasons

Issuer-side causes start after the request reaches the bank. The bank can decline a payment attempt for risk or policy reasons. The bank can also apply limits or blocks to a bank account or a card. Some payment issues come from authentication issues during regulatory steps. These failures can look inconsistent across issuers. A merchant needs clean logging to see the real pattern.

Merchant & system causes

Merchant-side causes happen when the payments setup isn’t aligned with the transaction. A misconfigured payment gateway can send incomplete or incorrect requests. Checkout technical errors can interrupt the flow before the bank sees the payment attempt. Currency mismatches can also cause declines or errors at the bank or payment processor. Some issues appear only on certain devices or browsers. Better monitoring helps teams spot these patterns early.

Why reducing failed payments matters for your business

Payment failure has a direct effect on growth and retention. Lost revenue shows up when a charge does not settle and the service cannot continue. Involuntary churn rises when a payment failure occurs during renewal and the customer does not fix it in time. The risk increases when retries are poorly timed or messaging is unclear. The impact compounds when failures repeat across multiple billing cycles.

Payment failure also shapes customer experience and trust. Customers often assume the merchant caused the issue when a payment failure occurs at checkout. Confusing prompts can reduce customer satisfaction even when the bank is the source of the decline. Clear, calm messaging helps meet customer expectations in a stressful moment. A smooth recovery flow protects customer experience and supports future purchases. It also reduces the chance that a customer abandons the brand after one bad attempt.

Operational costs rise when payment failure becomes a daily workload. Support teams handle tickets, refunds, and account reactivations. Finance teams spend time on reconciliation and exception handling. Risk teams review edge cases that could have been resolved earlier in the flow. Processing becomes less efficient when retries are unmanaged and outcomes are not tracked. Reducing failures lowers this load and frees teams for higher-value work.

How to reduce failed payments (step-by-step)

A failed payment is rarely a mystery when you track the full path from checkout to settlement. You can reduce failed transactions by fixing what you control before you ask a bank to approve anything. You can also improve failed payment recovery when a payment attempt fails for reasons outside your direct control.

This section breaks the work into five practical steps that fit most recurring payments and one-off checkouts. Each step reduces payment declines while protecting customer experience. Each step also supports business revenue by improving conversion and renewals.

Treat this as a loop rather than a one-time project. Your goal is fewer failures and faster recovery when payment failure happens.

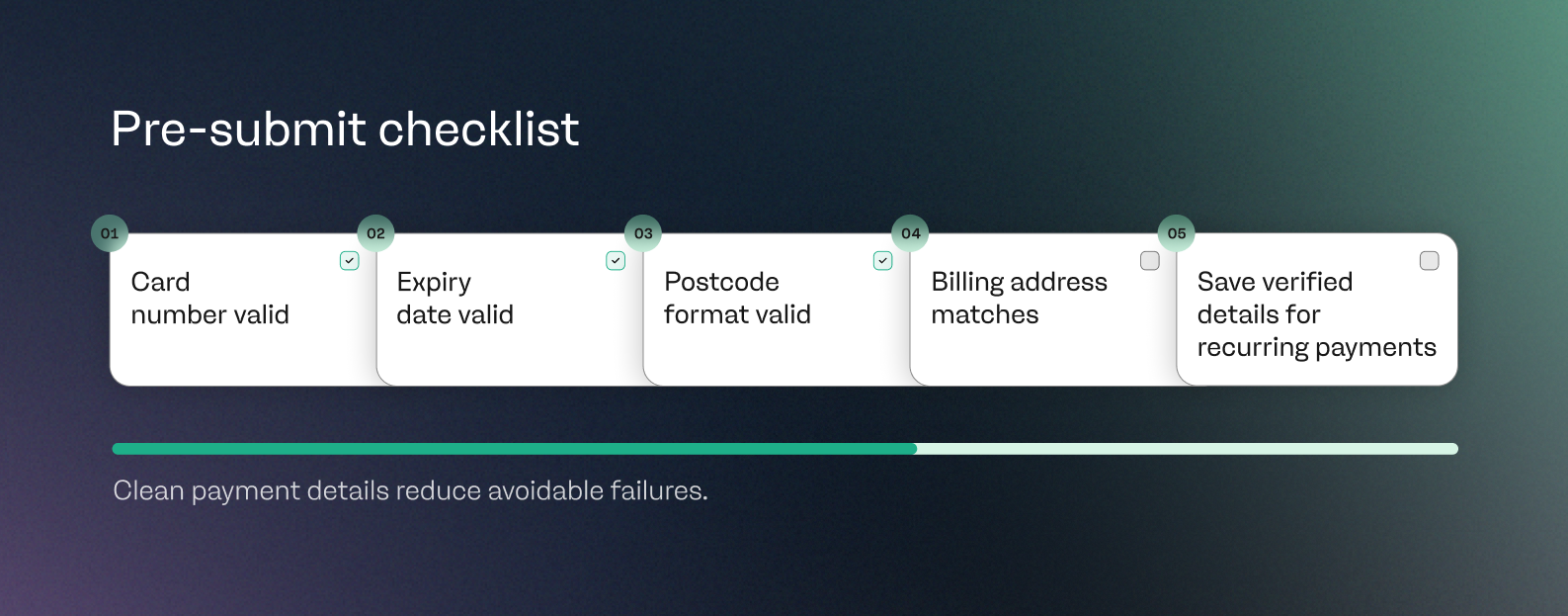

Improve data quality before submission

Data quality reduces avoidable failures before payment processing even begins. Validation catches mistakes before a bank has to decide what to do with them. This approach improves conversion because it prevents basic rejections. It also protects legitimate payments from being flagged as inconsistent. A merchant should aim to send clean payment details on the first attempt. That discipline reduces noise in decline data and helps you tune later steps.

Real-time validation is the simplest lever. Validate card number formats as the user types. Check expiry dates against the current month. Confirm postcode and address fields with reliable lookups. You can also detect a mismatched billing address before you submit the payment attempt. This reduces declines that stem from simple input errors. It also reduces friction because the user fixes issues in the moment.

Autofill and reduced form friction improve accuracy and completion. Autofill reduces typing errors for names and addresses. It also supports faster mobile checkouts. You should still confirm that autofilled values meet formatting rules. You can guide users with clear field labels and examples. Additionally, you can show inline error messages that explain one fix at a time. Further, you should keep error copy calm and specific. You can also save verified details for recurring payments when the user opts in. That approach reduces future failed transactions caused by repeated manual entry.

You should also standardise how you store customer data across systems. Inconsistent customer records can break token usage and mandate references. That inconsistency can create failures that look like payment declines. Logging should capture which fields failed validation and why. Logging should also capture which device and browser the user used. This context helps you find patterns in payment failure across segments. It also helps you prioritise changes that improve legitimate payments.

Before you roll changes out, define what “good” looks like. Your team should agree on a minimum data set for submission. Your team should also agree on what to do when data is missing. You can use progressive disclosure to ask only what you need and for more details only when risk or rules require it. That keeps the experience simple without weakening controls.

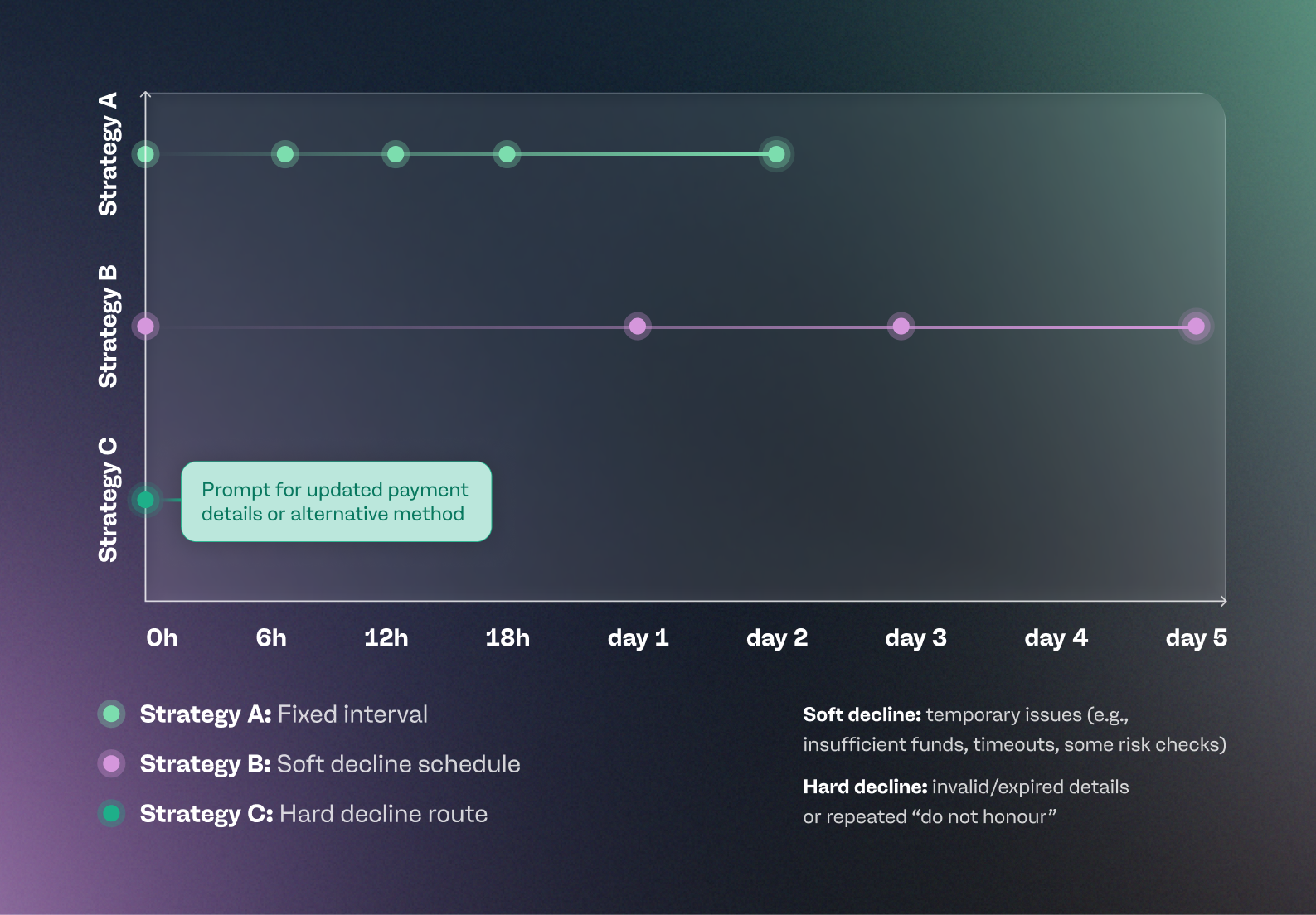

Intelligent retry logic

Retry logic is the core of failed payment recovery for recurring payments. It can also help one-off payments when the user stays in session. The key is to treat each outcome differently. Soft declines often resolve with time or a small change. Hard declines usually need new payment details or a different method. A single rule for all outcomes wastes payment recovery efforts. It can also increase issuer risk signals.

Start by separating soft and hard declines. Soft declines include temporary issues like insufficient funds. Soft declines also include time-out errors and some risk-based rejections. Hard declines include invalid credentials and an expired instrument. Hard declines also include explicit “do not honour” patterns that repeat. The bank often signals this difference through a decline code. The bank can also provide a network response that maps to your decline taxonomy. You should store the raw decline code, your mapped category, the attempt count, and the time between attempts.

Next, schedule retries with intention. A retry window should match the expected resolution pattern. Salary cycles often matter for insufficient funds. Weekend settlement patterns can matter for some bank account rails. Authentication windows can matter for some payment types.

You should avoid retry storms that hammer the same issuer in minutes. That pattern can reduce approval rates for legitimate payments. It can also increase the chance of a risk-based block.

Define a reasonable duration for recovery and specified period for each product or invoice type. A subscription renewal might use a shorter window than a high-value invoice. A trial conversion might use a shorter window than an annual plan. Document these choices so teams can explain them. This clarity also supports customer expectations. It helps support teams handle questions in a consistent way.

Use smart retry scheduling instead of fixed intervals. Start with a same-day retry only when the reason supports it. Use a next-day retry for many soft declines. Use a day-three retry for patterns that often resolve after funds refresh. Limit the total attempts to avoid excessive friction. Ask for updated details when the system sees a hard decline signal. Ask earlier when the same decline repeats. A long retry series without messaging can feel like a silent failure. A long series can also delay the point where the user takes action.

You should also align retries with your communication plan. A retry without notice can surprise a user. A notice without a retry can waste a recovery opportunity. Combine both so each step feels deliberate. Keep your copy clear about what will happen next and clear about whether the charge will repeat. This reduces complaints and chargebacks. It also protects customer experience.

Proactive notifications and dunning sequences

Dunning works best when it feels like help rather than pressure. The goal is to prompt the right action at the right time. The message should match the cause of the failed payment and also match where the customer is in the lifecycle. A trial conversion needs a different tone from a long-term subscription. A high-frequency service needs a different cadence from an annual plan. All of this supports failed payment recovery without harming trust.

Start with pre-dunning messaging. Pre-dunning means you warn the user before a renewal happens. You can send a reminder a few days before the charge, including the renewal amount and date. You can also include a direct link to update details. This reduces failed transactions caused by outdated credentials. It also reduces failures caused by an expired instrument. It can also reduce insufficient funds issues when users can plan. Keep the message short and factual, and the call to action obvious.

Follow up quickly after a failure. A first notice should confirm that the payment attempt didn't succeed. The notice should also confirm whether service continues for now and explain the next action you will take. Further, it should explain what the user can do now. This message should also avoid blame. Many payment declines come from issuer controls the user cannot see. A calm message protects customer satisfaction.

Personalisation improves outcomes when it stays respectful. Include the product name and renewal date. Share the amount and currency. Reference the last four digits of account numbers like debit or credit card numbers only when appropriate. Avoid exposing full payment details. Provide an in-app path and a web path. Offer a clear option to switch methods when there's support for multiple payment methods and alternative payment methods. Some users will fix the issue faster if they can choose a wallet or use a bank account method. Give options without adding noise.

Build a sequence with a clear end point. Define the specified period for reminders and what happens when the period ends. Explain whether access pauses or downgrades, whether you will cancel, and how reinstatement works. Keep the timeline predictable. Predictability supports customer expectations. It also reduces disputes when a user misses a message.

Clear communication of grace period terms helps manage customer expectations. It also reduces confusion about payment deadlines. State the grace period length in plain language. Confirm the exact date when access changes. Explain what happens during the grace period. This keeps the timeline predictable for the customer.

Dunning can be a positive experience when it feels like guidance. It can improve client retention when the next step is obvious. It can also support better communication with customers. Use friendly copy that focuses on restoring service. Offer one clear action in each message. Confirm when the next payment attempt will happen. This approach keeps trust intact while you recover revenue.

Offer multiple and local payment methods

Choice reduces friction when the original method fails. It also reduces abandonment when users cannot fix a card quickly.

Multiple payment methods help you recover revenue without forcing the user to leave. They also reduce the impact of local preferences. Some markets prefer cards. Other markets prefer wallets. Some markets prefer bank-based payments. Offering alternative payment methods can lift conversion for new users. It can also improve renewal success for recurring payments.

Start with digital wallets where they fit your audience. Wallets reduce manual entry and improve data accuracy. Wallets can also reduce payment issues tied to card number entry. They can support biometric confirmation on mobile. They can also reduce the chance of a mismatched billing address. Use wallets as a first-class option rather than a hidden fallback. Surface them early when users choose how to pay. Keep the option list short and relevant.

Add local methods based on market fit. Bank transfer and direct debit can work well for some subscriptions. Account-to-account options can reduce card expiry problems. They can also reduce payment declines tied to issuer risk models for cards.

A bank account method can fit higher-value invoices. It can also fit B2B use cases. Make sure you understand mandate and confirmation requirements. Make sure your user journey explains what the user authorises. Clarity reduces confusion and disputes.

Method routing also matters. A method that works in one country may underperform in another. A method can also perform differently by device. Track conversion by method, country, and issuer range. Track renewal success separately from checkout success. This shows where method coverage helps most. It also shows where you should add or remove options.

Method choice must still stay simple. Too many options can reduce completion. Group methods by type where possible. Use clear labels users recognise and short helper text when a method has a different settlement feel. That helps users choose confidently. Confidence supports future purchases and customer satisfaction.

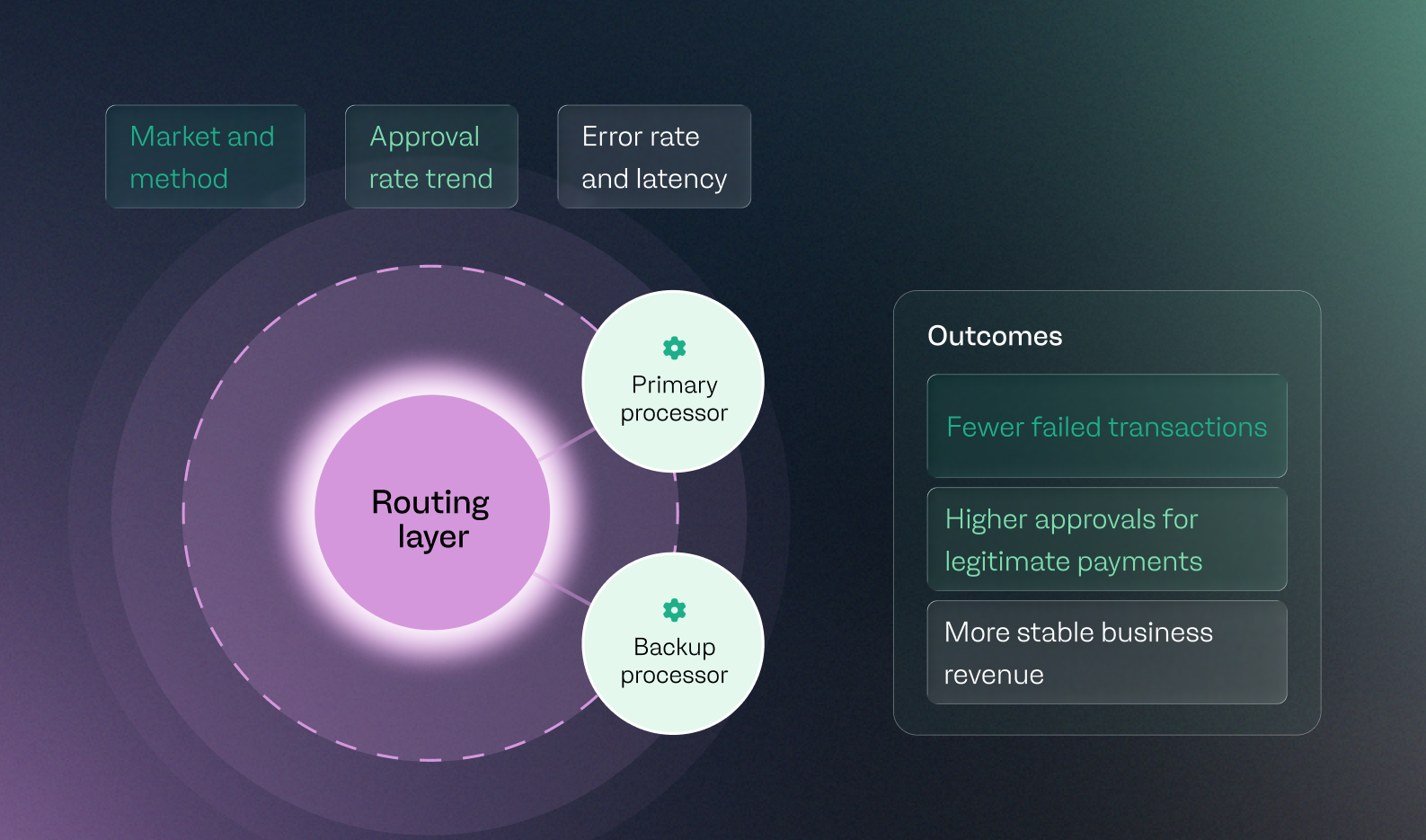

Use multi-processor strategy

A single path can create a single point of failure. A multi-processor strategy reduces downtime risk. It can also improve approvals in specific regions and performance for certain issuer groups. This strategy can protect business revenue during outages. It can also reduce silent losses from degraded routing. It is most useful at scale and for merchants with international coverage.

Start with a clear fallback plan. Set your primary route for each market and choose a backup route. Specify when you will fail over and who can trigger changes. Agree how you will monitor performance. Monitoring should include approval rate, error rate, latency, and settlement success.

Geographical performance drives many wins. Some processors have stronger coverage in certain markets, better issuer relationships in certain corridors or stronger support for certain methods. Use data to guide routing decisions. Use controlled tests rather than broad switches. Keep a holdout group for comparison. This avoids confusing normal variance with a real uplift.

Keep compliance and reporting aligned across routes. Data fields can differ across processors and status naming can differ across systems. Reconciliation can also become harder if you do not standardise. Build a normalised event model. Store raw responses for audits and debugging. Store your mapped categories for reporting. This makes payment processing easier to manage across providers. It also makes payment recovery efforts easier to track.

Multi-processor also needs clear customer messaging. Users should not see confusing differences between attempts. Your checkout and receipts should look consistent. Similarly, your billing descriptors should be stable where possible. Consistency protects trust. It also reduces support contacts.

Tools & technologies to reduce failed payments

Payment orchestration platforms sit between checkout and payment systems. They route each transaction request through the best available path. Orchestration also helps you accept payments across payment channels without rebuilding every integration. It standardises payment information before submission, reducing errors caused by incorrect payment details. It also helps when a credit card fails.

Analytics and reason code dashboards turn a failed payment into a clear cause. They connect outcomes to segments like issuer, country, device, and payment channels. These dashboards highlight spikes in incorrect payment details and flag gaps in payment information. They also show when risk rules block legitimate transactions. This visibility helps you tune fraud prevention. It also helps you separate suspected fraud from data-quality problems.

Automated retry and recovery tools improve outcomes after a failed payment. They trigger retries only when the decline pattern supports another attempt. Recovery tools prompt users to update payment information when the signal points to incorrect payment details. They also guide users to switch methods when recovery is unlikely with the current credit card. These tools reduce noisy retries across payment systems and protect legitimate transactions during recovery.

For a practical way to reduce failed payment rates while keeping your checkout stable, payabl. can help you accept payments across payment channels and improve recovery.

Summary: key takeaways on reducing failed payments

Failed payments cost money because they interrupt cash flow and add recovery work. Not all failed payments have the same cause or the same fix. Card payments can fail for issuer decisions, customer-side problems, or technical issues in your stack.

Recurring billing improves when you combine clean data, smart retries, and clear recovery journeys. Automated notifications help customers act quickly and reduce silent churn while creating a positive customer experience. You can route transactions more effectively when you use reason codes and performance signals. International purchases benefit from local methods and strong routing because issuer behaviour varies by market. The goal is to turn payment failure into successful transactions with fewer steps and less friction.

If you want to reduce failed payments with practical tooling, start with payabl. as your gateway provider for online payment acceptance and routing. If your flow also needs fast outbound movement of funds, use payabl. payouts to send money to recipients through local rails.

For day-to-day treasury and settlement control, payabl. offers accounts for business with multi-currency capabilities. If you also take in-person payments, payabl. provides POS terminals that connect in-store and online acceptance.

For implementation detail, use the documentation on declines and failed payments to interpret outcomes and improve recovery logic. For method-specific troubleshooting, use the alternative payment method error codes reference to map issues quickly.

FAQs about failed payments

What does payment failed mean?

It means the charge didn't complete and the payment didn't settle. A declined transaction can happen if the issuing bank rejects the request, or if the customer’s account details don't pass checks. It can also happen when there aren’t enough funds in the customer’s account at the time of the attempt.

What is the impact of failed payments on a business?

Transaction failures can trigger a ripple effect that erodes brand loyalty over time. Customers can lose confidence after repeated transaction failures and may switch to a more reliable alternative. The most direct impact is immediate lost revenue, which reduces customer lifetime value and slows overall business growth.

How can businesses manage failed payments without making things worse?

Most transaction failures come from incorrect payment details, insufficient funds, or an expired card. Some declines come from an issuing bank security block based on risk signals and payment preferences. Use a structured approach to reducing payment failures with validation, clear prompts, and a smart retry plan. Avoid aggressive retries because repeated attempts can trigger fraud prevention measures and lead to an account freeze or card restriction.