When businesses accept digital or credit card payments, they rely on payment gateways and payment processors to handle the core steps of payment processing. Both play crucial but distinct roles in securely transmitting payment information and moving funds between a customer’s and a merchant’s bank account.

A payment gateway collects and encrypts customer payment data at checkout, while a payment processor authorises transactions and facilitates fund transfers between the issuing bank and the merchant’s acquiring bank.

Understanding the payment gateway vs payment processor difference is key to selecting the right solution and avoiding costly integration mistakes.

What is a payment gateway?

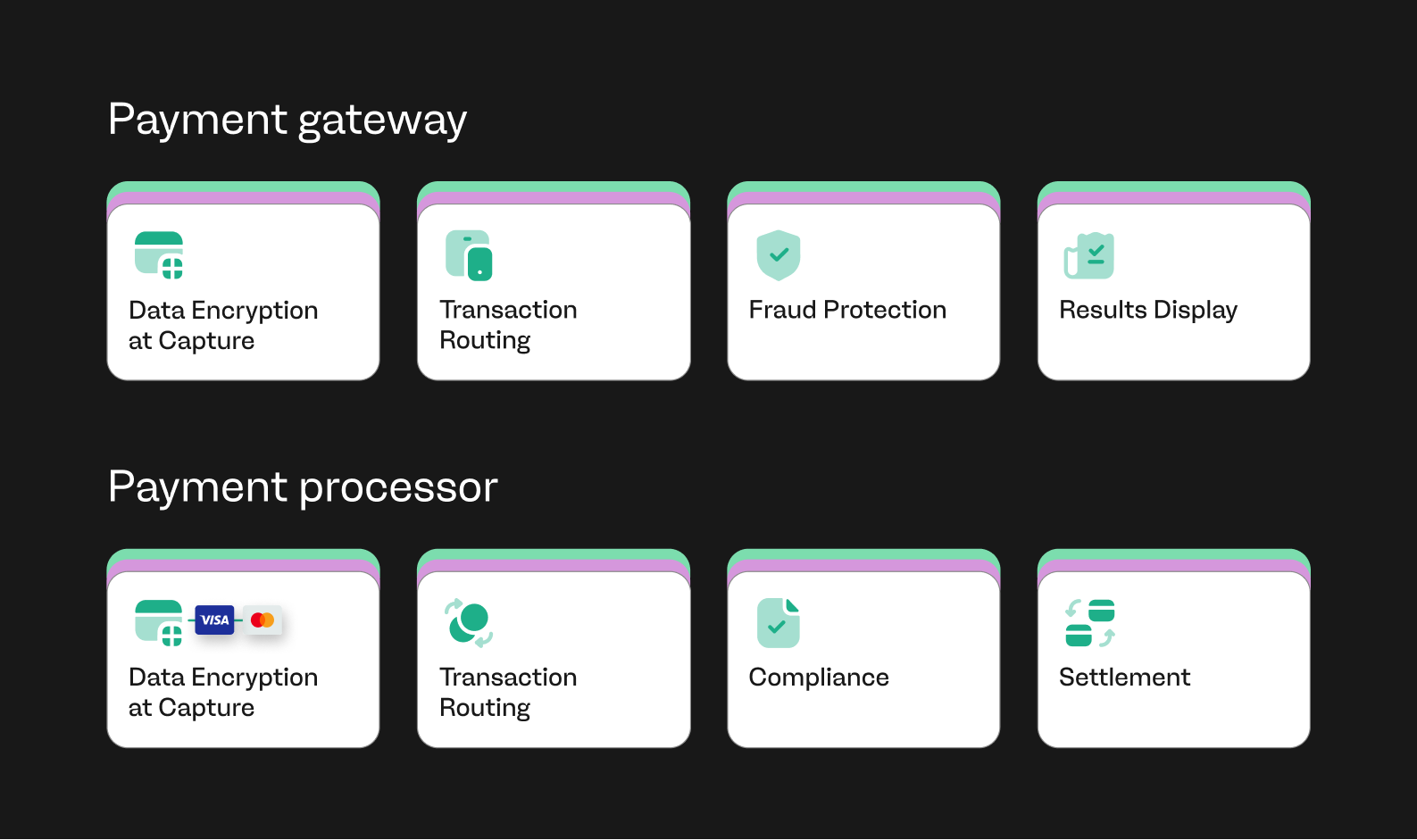

A payment gateway is the customer-facing component that securely captures credit card or debit card details at checkout. The payment gateway encrypts the sensitive information, performs initial fraud screening, and transmits transaction data to the processor for authorisation. It acts as the interface between customers and back-end payment systems.

Security is the primary function of payment gateway software. By securely transmitting payment information and tokenising credit card data, the gateway helps reduce PCI DSS burdens for merchants.

Modern payment gateway providers, such as payabl., offer integrated payment gateway services that support more than 300 digital payment methods, including cards, bank transfers, and other digital payment methods. These gateways feature hosted payment pages, direct API integrations, mobile and web SDKs, plugins and payment links, allowing online stores to accept payments securely without exposing sensitive payment data.

What is a payment processor?

A payment processor operates behind the scenes to authorise and settle payment transactions. After receiving encrypted data from the gateway, the payment processor acts as an intermediary, routing authorisation requests through credit card networks such as Visa or Mastercard to the customer’s card issuing bank.

Once approved, the payment processor facilitates fund movement between the issuing bank and the merchant’s acquiring bank. Payment processing services maintain direct connectivity with card networks to reduce latency and increase transaction approval rates. Additionally, processors handle chargeback management, compliance, and reporting for merchants.

Payment gateway vs payment processor: key differences

Feature | Payment gateway | Payment processor |

| Role | Payment gateway collects and encrypts card data, sends for authorisation, and returns the result to the merchant. | Payment processor receives data, routes through credit card network, manages clearing and settlement. |

| Key functions | Checkout UI, encryption, tokenisation, 3D Secure, basic fraud checks. | Compliance management, clearing, settlement, reconciliation, reporting. |

| Customer visibility | Customer-facing at checkout for online transactions. | Operates in the background, invisible to customers. |

| PCI compliance scope | Reduces merchant PCI exposure. | Must maintain PCI DSS compliance. |

| Integration | Sometimes requires integration with the merchant's POS system or ecommerce platform. | Set up by merchant service provider or payment service provider. |

Functional differences explained

- The payment gateway encrypts data at capture; the payment processor vs gateway distinction shows that the processor routes approved transactions through card networks.

- Gateways handle user-facing checkout and store payment details; processors handle transaction processing and fund movement.

- Gateways provide enhanced fraud protection and initial checks, while processors enforce compliance and money services business regulations.

- Gateways display transaction results to merchants; processors ensure final settlement to the business’s bank account.

Who needs which?

For most merchants, the answer in the gateway vs payment processor debate is “both.”

- Ecommerce stores need gateways to manage checkout and processors to accept credit card payments.

- SaaS companies should choose integrated payment gateways supporting tokenisation for recurring charges.

- Physical retailers using a credit card reader, POS system, or credit card machines perform gateway functions at hardware level but still require a processor to complete in person transactions.

- Multi-channel businesses benefit from unified payment solutions that combine both functions and provide consolidated reporting.

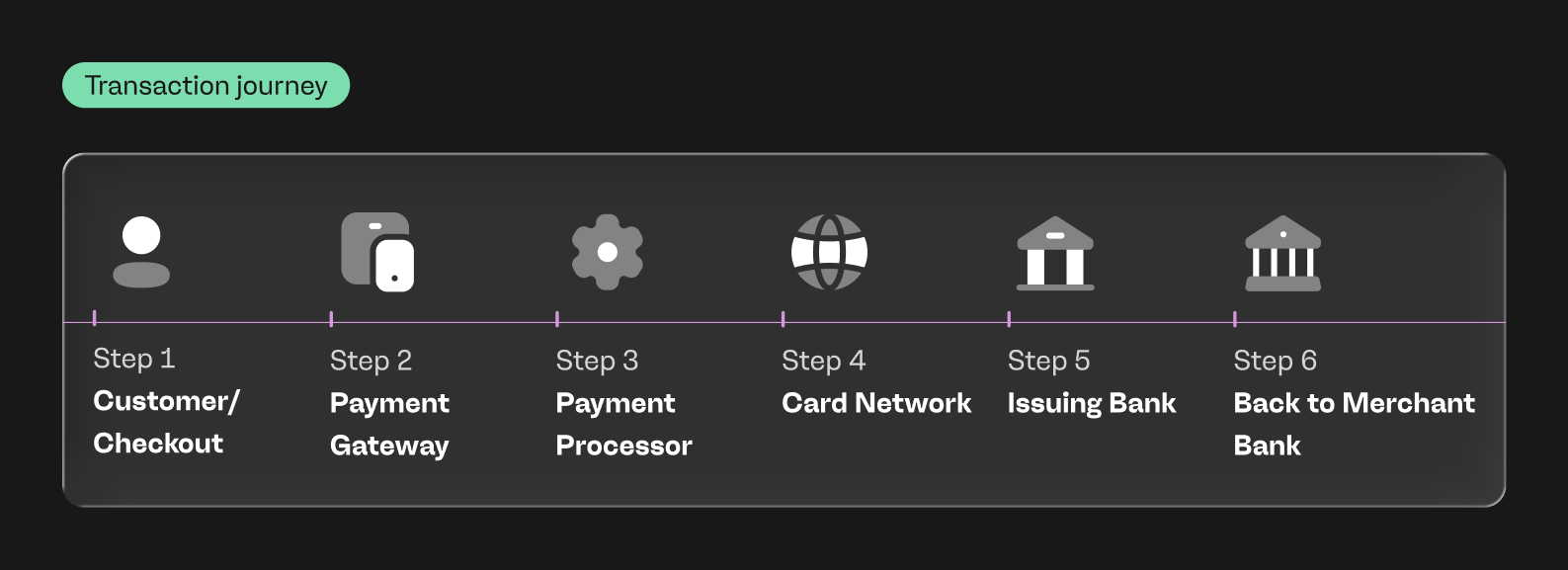

How payment gateways and processors work together

- Customers enter payment details on an online store or app.

- Payment gateway encrypts and validates the customer’s credit card information.

- Payment gateway transmits the data to the payment processor.

- Processor routes request through the appropriate credit card network.

- The issuing bank approves or declines the credit card transaction.

- The processor relays results back to the payment gateway, which notifies both merchant and customer.

- The payment processor facilitates clearing and transfers funds to the merchant account.

Payment gateway vs payment processor examples

Some merchant account providers integrate both functions, while others specialise.

- All-in-one solutions like Stripe, Adyen, and Square combine payment gateway and processor roles into one platform, enabling merchants to process payments seamlessly.

- Third party payment gateways (like PayPal's Payflow Pro) can also connect to external processors, giving merchants flexibility to negotiate fees or switch processors without altering the front-end gateway.

These integrated or modular setups reflect different business needs and technical preferences in payment processing services.

Costs & fees: what to expect

Payment gateway and payment processor fees are typically structured separately, though all-in-one providers can bundle these costs.

Fee components

Typical costs for payment processing include:

- Transaction fee (2–3%)

- Fixed fee per transaction ($0.30–$0.49)

- Monthly gateway fee (up to $30 for standalone payment gateway providers)

- International card markup (1–1.5%)

- Variable rates for foreign credit cards, digital wallets, or local payment methods

High-volume businesses can negotiate custom pricing with merchant service providers or payment processors offering interchange-plus models.

Common fee scenarios

Standard ecommerce transactions through providers like Stripe or Square typically cost 2.9%, plus $0.30 per successful charge. High-volume merchants may negotiate custom rates with volume discounts. Low-volume businesses often benefit from pay-as-you-go models without monthly minimums.

Interchange pricing models charge an interchange rate, plus a fixed markup (typically 0.5% plus $0.25). This transparent structure can reduce costs for businesses with predictable transaction volumes.

How to choose the right option for your business

Factors to consider

When comparing payment processor vs payment gateway, consider:

- Required payment methods (credit, debit, local alternatives)

- Integration needs (plugins vs custom APIs)

- Merchant account and settlement speed

- Compliance and enhanced fraud protection tools

- Support for tokenisation, recurring billing, and multi-currency capabilities

Providers like payabl. offer flexible payment gateway services with robust APIs and risk management features tailored to complex merchant needs.

Checklist

- Identify required payment methods (cards, digital wallets, bank transfers, local options)

- Assess technical resources for integration and maintenance

- Calculate total cost based on projected transaction volume and average order value

- Verify PCI compliance support and security features

- Confirm availability of required features like subscriptions, tokenisation, fraud tools

- Evaluate reporting and reconciliation capabilities

- Check settlement timeframes and payout flexibility

- Review support model and availability for your business hours

- Test checkout user experience and conversion optimisation features

- Validate compatibility with existing ecommerce platform or business systems

Conclusion: which should you choose?

Most online businesses require both payment gateways and payment processors to accept card transactions securely.

Choosing between integrated payment gateways and standalone payment processors depends on business model, geography, and transaction volume.

Solutions like Stripe, Adyen, and Square combine both a payment processor and gateway, providing simplicity and scalability. Platforms like payabl. specialise in gateway vs payment processor solutions that support global payment methods, enhanced fraud protection, and fast integration for businesses looking to accept credit cards and optimise conversion.

FAQ

Is one better than the other?

Payment gateways and payment processors serve different functions rather than being competing alternatives. Gateways handle customer-facing payment capture and encryption, while processors manage authorisation and fund movement. Both components are necessary for complete payment processing capability.

Does my business need both?

Online businesses need both gateway and processor functions to accept digital payments. These functions may come from a single integrated provider or separate specialised services. Physical retail locations using point-of-sale terminals still require processor connections, though the terminal hardware often performs gateway encryption functions.

Can a company be both gateway and processor?

Many modern payment companies combine gateway and processor capabilities in a single platform. Stripe, Adyen, and Square all function as integrated providers, offering both payment capture interfaces and processing services. This simplifies merchant onboarding and reduces the complexity of managing multiple provider relationships.