Thinking about building your own payment gateway solution to accept debit and credit card payments?

Online payment gateway development requires deep expertise in payment processing and strict integrations with multiple financial institutions to power online transactions.

When researching how to build a payment gateway from scratch, you’ll quickly discover the complexity behind developing secure and compliant online payment flows. This guide outlines the specific steps you need to follow, as well as alternatives to building a gateway completely in-house.

Why consider building your own payment gateway system

Exploring the possibility of in-house payment gateway development can be appealing if you want to gain tighter control over your payment processing stack and customise your gateway features.

Choosing to create a payment gateway can potentially offer you greater flexibility across digital payments, credit and debit card payments, and your online payment flows. However, building a full payment gateway solution that integrates directly with payment processors and financial institutions is no small task and requires weighing the benefits against the drawbacks to decide whether it’s the best option.

Reasons to develop your own payment gateway

- Increase your control over payment data: Engaging in online payment gateway development allows you to precisely define how data is stored, routed and secured across all of your online transactions. It can also reduce your reliance on external providers and align your system with the specific requirements of the financial institutions you work with.

- Lower long-term costs and transaction fees: Creating a payment gateway from scratch gives you the freedom to optimise your payment processing flows and reduce recurring transaction fees. You can avoid payment service fees that build up over time by streamlining those costs through your in-house operations.

- Brand your payment experiences: Many businesses that research “how to create my own payment gateway solution” do so with the goal of customising the branding of their payments. Building a gateway entirely in-house gives you the opportunity to customise interfaces and workflows, and to provide customers with a branded journey across all digital payments.

- Support for multiple payment methods: When you build your own payments stack from the ground up, you can imbue your system with the capabilities needed to accept a wide range of payment methods based on your customer preferences and regional requirements.

Who needs their own payment gateway?

- Financial institutions: Banks, insurance companies, and other financial entities may want to pursue payment gateway development as a way to gain full control over payment processing. An in-house gateway can ensure these organisations’ digital payments ecosystems align with their specific regulatory and operational needs.

- Large ecommerce enterprises: If you are a high-volume merchant, you may choose to build your own payment gateway so that you can customise checkout flows, reduce payment processing costs, and optimise your payment performance at scale.

- Corporate enterprises: Huge companies with complex infrastructures often explore how to develop a payment gateway system to unify their global payment streams. Like ecommerce enterprises, an in-house gateway can be the key to reducing costs and improving performance.

- Government agencies and non-profits: These types of organisations may create a payment gateway to enhance trust with their users. An in-house gateway can also provide a more streamlined method for achieving financial transparency and compliance within a specialised payment gateway environment.

Main challenges and risks of a custom payment system and gateway

- Regulatory complexity: Custom payment gateway development must comply with strict regional and global standards, adding time and expense to every stage of the transaction process. This can also significantly complicate development timelines, as you must perform the necessary checks and regulatory certification processes.

- High upfront and ongoing costs: Building your own gateway requires substantial upfront investments, as well as ongoing maintenance and update expenses to keep a reliable payment processing system operational long after initial development is complete.

- Integration challenges: Connecting your payment gateway to a payment processor and an acquiring bank adds technical and operational complexity. On top of these integration needs, you must also obtain a merchant account and the required credentials without the help of a third party.

- Security risks: A proprietary payment gateway requires you to have a thorough understanding of payment risks and how to protect your system against them. You need advanced security mechanisms for detecting and preventing fraud, breaches and data leaks.

5 questions to ask your CTO:

- Do we have the required expertise?

- What is the full cost of development?

- How will we handle compliance?

- Can we support long-term maintenance?

- Are in-house integrations with financial institutions feasible?

So, if you do have expertise and manpower ready, you can handle the compliance needs, and maintain software, then you can consider in-house development.

Payment gateway architecture and core components

High-level architecture overview

Understanding how to build a payment gateway architecture ensures that every component can work together reliably and at scale.

A high-level overview of a gateway architecture includes the API layer, orchestration engine, security modules, and bank integrations. It should define how data flows between the front-end checkout interface to the back-end services, as well as how it connects to payment processors.

As you create a payment gateway that is custom to your business, you must develop a core system that can securely capture payment details and route transactions intelligently. A comprehensive payment gateway design will also manage critical functions like authentication, fraud checks, and integration with your merchant account for handling tasks like fund settlement.

Front-end checkout integration

Front-end checkout integration is a critical step when you create a payment gateway. It shapes customers’ online payment experiences across all your digital channels, from your website to your mobile app.

Your developers must create a UI that is intuitive, fast, and accessible across devices while exposing a clean, well-documented API that supports secure data capture and flexible workflows. The payment portal you develop should provide real-time validation and gracefully guide users through errors, all while maintaining a high degree of security from the first click of every transaction.

For businesses dealing with transactions in multiple currencies and regions, you need a front-end interface with capabilities like multi-currency price display, localised fields, and adaptive formatting based on the geographic location of the customer and payment.

In terms of mobile optimisation, you must develop layouts specifically for mobile devices that feature responsive components based on the type of device in use.

Back-end processing

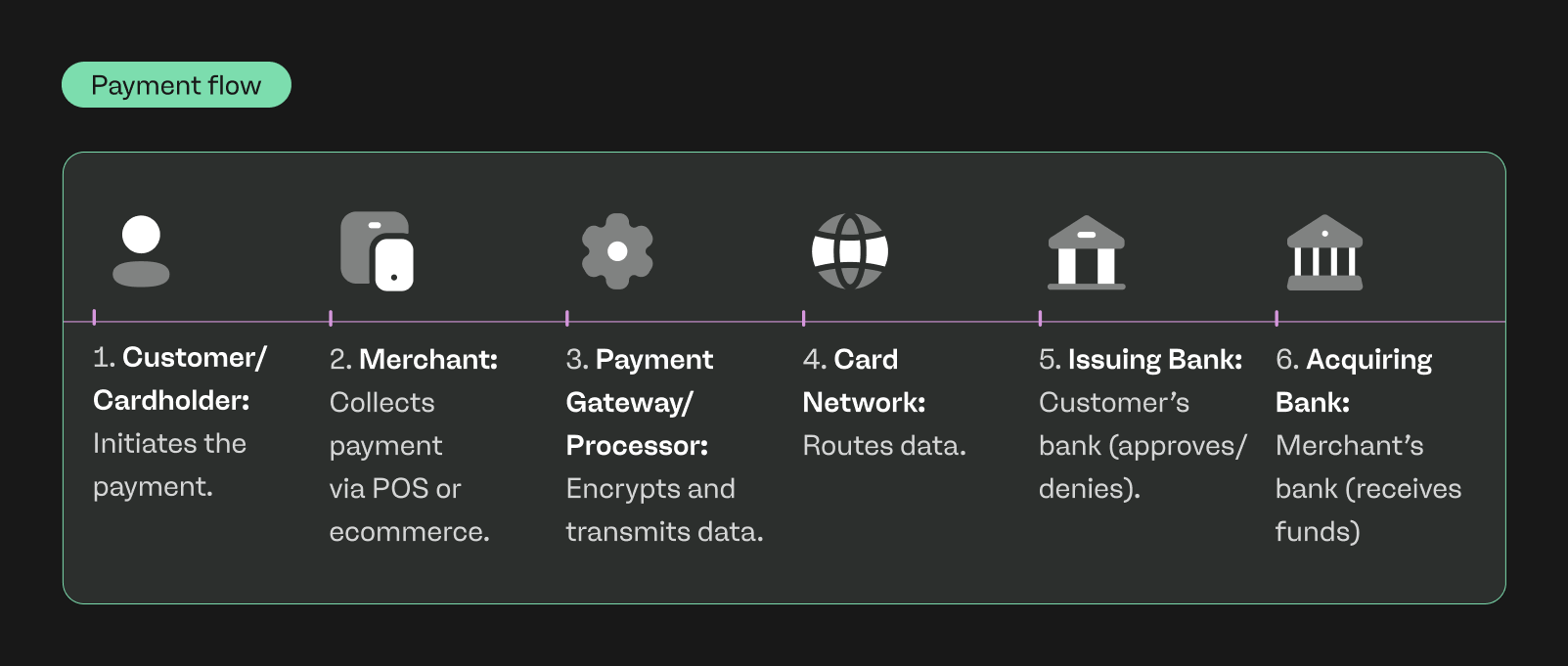

Back-end processing is the core engine of any payment gateway, defining the logic that determines where each transaction is routed. This logic is combined with your business relationships with payment processors and acquiring banks to manage the full transaction process, from authorisation to fund capture.

After funds are validated and sent through the pipeline, your system needs the ability to automatically perform reconciliation to match successful payments so that the funds can be settled from your merchant account into your business bank account. You also need thorough reporting capabilities that can provide detailed insights into payment approvals, declines, transaction fees and chargebacks.

Security and risk layer

The security and risk layer of a custom payment gateway is responsible for protecting payment data from customer initiation to payment approval and settlement.

Your security layer should include tokenization to protect this data, which can be decrypted only once it reaches your acquiring bank and the customer’s issuing bank. You will also need to develop and implement advanced fraud prevention tools to analyse risk signals in real time, as well as integrate comprehensive KYC processes to verify user legitimacy.

A secure payment gateway must also authenticate transactions before passing them to the designated payment processor so that all online payments meet regulatory and network requirements.

Step-by-step process for how to build a payment gateway with cost estimates

Building a payment gateway requires a structured approach, complete with significant resources and a high level of technical expertise from your developers.

In this section, we break down the full payment gateway development lifecycle to show what it truly takes to build a custom payment gateway. Each step highlights realistic timelines, staffing requirements, and risks to demonstrate what shapes a production-ready payment gateway project.

| Step | Timeline | Team required | Risks |

| Step 1: Feasibility and business requirements | 2 to 4 weeks |

|

|

| Step 2: Design and architecture planning | 3 to 6 weeks |

|

|

| Step 3: Tech stack and infrastructure | 4 to 8 weeks |

|

|

| Step 4: Development and API integration | 8 to 16 weeks |

|

|

| Step 5: Compliance and security testing | 4 to 8 weeks |

|

|

| Step 6: Go-live and continuous optimisation | Ongoing |

|

|

Step 1. Feasibility and business requirements

The first step in building a payment gateway is evaluating feasibility and defining clear business requirements. You must outline your specific goals, target transaction volumes, and compliance scope, keeping in mind key considerations like PCI DSS compliance, local regulations, and KYC. During this step, you must also consider how your payment gateway will interact with each payment processor to ensure smooth and secure transaction flows.

Requirements:

- Staff: Must include at minimum business analysts, project managers, and compliance specialists. However, your ideal step one team should also include developers, security specialists, and operations personnel.

- Budget considerations: Planning, research, and preliminary assessments.

- Timeline: Typically takes around a month, with multiple meetings and planning sessions.

- Risks: Poor communication between planning teams can lead to misaligned goals, underestimated budgets or transaction volumes, and regulatory oversights.

Step 2. Design and architecture planning

In this phase of building a custom payment gateway, you must define the overall system architecture and plan your integrations with acquiring banks, payment processors, and merchant platforms.

Choosing an architecture type (such as monolithic, microservices, or hybrid) can affect multiple functional aspects of your payment gateway, including scalability, security, and performance. Detailed planning ensures your payment gateway can efficiently handle critical tasks like transaction routing, reconciliation, and reporting.

Requirements:

- Staff: Solution architects, back-end engineers, security experts, and QA testers

- Budget considerations: Infrastructure, software licenses, and integration costs.

- Timeline: Can take 3 to 6 weeks to complete the architecture design, approvals, and integration planning.

- Risks: Integration failures, scalability bottlenecks, and misalignment with compliance requirements.

Step 3. Selecting a tech stack and infrastructure from the payment gateway market

When choosing your payment gateway tech stack, you need to consider what programming languages, frameworks, and databases are best suited to your needs. You’ll also need to decide between a cloud-based or on-premise infrastructure, with the former requiring a cloud services vendor and the latter demanding substantial hardware and resources.

The specific technologies and programming languages you use will depend on what you want to achieve in terms of features and capabilities. Examples of common back-end languages include Java, Node.js, or Python. For front-end coding, you’ll need the standard HTML and CSS languages, along with additional frameworks for more complex designs, like Vue.

Requirements:

- Staff: DevOps engineers, back-end/front-end developers, and security specialists

- Budget considerations: As you choose your frameworks and languages, you’ll need to consider the cost of development licenses, hosting, cloud services, and monitoring tools.

- Timeline: Setup, testing, and deployment can take between 4 to 8 weeks.

- Risks: Performance bottlenecks, tech incompatibility, and vendor lock-in.

Step 4. Development and API integration

During development, your teams must build the core modules of a custom payment gateway, including transaction routing, authentication, tokenization, and reconciliation. During this step is when you will integrate acquirers and payment processors.

Developers may explore multiple approaches depending on the tech stack, requiring you to research:

- How to develop payment gateway in Java

- How to develop payment gateway in Python

- How to develop payment gateway in C#

- How to develop custom gateway in PHP

Also during this stage is when you must research critical questions about how to create your own payment gateway from scratch, with a specific focus on reliability, security, and scalability.

Requirements:

- Staff: Backend engineers, integration specialists, and QA testers

- Budget: Development tools, API access fees, and testing environments can stack up costs quickly, on top of the cost of paying development teams.

- Timeline: From module development to final integration, this step can take the longest amount of time between 8 to 16 weeks.

- Risks: API incompatibility, bugs, and delayed certifications

Step 5. Compliance and security testing

You must ensure your custom payment gateway is secure and compliant before launch.

This step includes implementing strong encryption and tokenization mechanisms, as well as figuring out how you want to handle and store sensitive data cross your payment processing system.

Instruct your teams to perform extensive sandbox testing to simulate real-world payment data flows, uncover vulnerabilities, and verify transaction accuracy. Achieving PCI DSS certification validates that the payment gateway meets industry standards and is a requirement for compliance.

Requirements:

- Staff: Security engineers, compliance specialists, and QA testers

- Budget considerations: You’ll need to account for certification fees, security tools, and testing environments.

- Timeline: Security implementation, testing, and certification can take anywhere between 4 to 8 weeks, though it may take longer to complete if you have to go through any remediation steps during certification.

- Risks: Non-compliance, data breaches, and delayed certification

Step 6. Go-live and continuous optimisation

Launching a payment gateway is just the beginning.

After going live, ongoing monitoring, performance tuning, and feature updates are necessary to ensure reliability and scalability. Continuous optimisation involves analysing transaction success rates, latency, error logs, and user feedback to improve the payment gateway experience. You must also stay updated on compliance changes, emerging fraud patterns, and new payment methods to maintain competitiveness.

Requirements:

- Staff: Operations engineers, support staff, and analytics team

- Budget considerations: Ongoing costs can include monitoring tools, maintenance, and updates.

- Timeline: There’s no definitive timeline for this final step, as you must engage in ongoing maintenance after the initial launch to make iterative improvements.

- Risks: System downtime, evolving security threats, integration issues

Payment gateway development costs, timeline and ROI expectations

Estimating the true cost of building a payment gateway requires you to understand every layer of the payment processing system, from the back-end architecture all the way to long-term maintenance.

In this section, we’ll provide a more realistic and detailed look into the costs and ROI expectations to determine whether custom development is worth the investment or if partnering with a third-party provider makes more sense financially for your company.

How much does it cost to build a payment gateway and key cost drivers

Calculating your budget for the payment gateway cost to build will vary widely depending on your technical scope, compliance requirements, and long-term operational needs. Below, we have detailed key cost drivers that influence the total investment required to develop a fully functional payment gateway:

- Feature complexity: Advanced capabilities like fraud detection, tokenization, multi-currency routing, and dashboards for monitoring and reporting can significantly increase development costs and testing requirements.

- Development team size: Larger, more specialised teams (like architects, back-end engineers, DevOps, QA, and security experts) can directly impact your total cost

- Compliance and certification: PCI DSS audits, encryption, penetration testing, and maintaining data protection standards add substantial extra, but necessary, expenses.

Estimated costs by project scope

| Project scope | Description and features | Estimated timeline from start to finish |

| Basic MVP payment gateway | A minimal product designed to validate core functionality. Includes basic transaction routing, simple APIs, limited fraud checks, single-currency support, lightweight reporting, and essential security. Intended for more simple payment processing rather than high-volume or multi-region processing. | 3 to 6 months |

| Enterprise-grade payment gateway | A fully scalable, production-ready gateway built for global operations. Includes advanced orchestration, multi-currency and multi-acquirer routing, real-time fraud systems, tokenization, dispute workflows, detailed analytics, and full compliance support. Designed for large merchants, financial institutions, and high-volume online payments.

| 9 to 18+ months, with additional timeline considerations for more complex compliance certifications |

ROI and break-even analysis

Evaluating ROI for a custom payment gateway depends on your development cost, transaction volume, operational savings, and reduced third-party fees. Businesses typically recover costs by eliminating per-transaction gateway markups and lowering long-term processing expenses.

For example, if a company saves $0.05 per transaction and processes 1 million transactions annually, that’s $50,000 recovered each year. Higher volumes can accelerate your break-even rate and ROI. For instance, processing 5 million transactions at the same savings yields $250,000 annually. If the initial payment gateway investment is $500,000, break-even could occur in 2 to 3 years at a moderate volume or under 12 months at enterprise scale, depending on feature scope and ongoing maintenance costs.

Build vs. buy vs. hybrid approach

Choosing whether to build or buy a payment gateway requires you to weigh the potential costs and decide what is best for your business model and technical capacity. You can also opt for a hybrid approach that combines building some elements in-house and working with service providers to build more complex technologies and technical components.

| Approach | Pros | Cons |

| Build |

|

|

| Buy |

|

|

| Hybrid |

|

|

When building in-house makes sense

Building internally is most effective when you have highly custom needs, a massive transaction volume, and a long-term focus on performance and scalability.

If you require proprietary routing and specialised compliance frameworks, the full ownership and control and in-house build can provide you with is ideal.

When buying or white-labeling is better

Purchasing a white-label or ready-made payment gateway is preferable for companies seeking a fast market entry with lower upfront costs and minimal operational complexity. This approach eliminates the burden of having to build your own compliance support in-house and can also make maintenance and integration processes far simpler compared to managing them internally.

If you’re looking for a fast, cost-effective solution without the developmental headache, payabl.checkout and the payabl.one platform can give you all the tools and support you need.

Hybrid solutions

A hybrid model blends together existing gateway solutions with your own proprietary logic, allowing you to customise your payment gateway solution while avoiding full development costs.

Regulatory and security considerations

Every payment gateway project must prioritise compliance and adhere to the strict regulatory standards that govern the payments industry. Because payment systems handle sensitive data, you must employ robust security measures that uphold the regulatory expectations of both local and global standards.

Core regulations and standards

Ensuring compliance across different regulatory frameworks is essential for any payment gateway handling sensitive payment data. The core regulations and standards to focus on include:

Below is a checklist of the top compliance steps before launch:

- Complete PCI DSS certification

- Implement encryption and tokenization

- Validate your KYC and AML workflows

- Review GDPR and regional data laws

- Run regular penetration tests and security audits

PCI DSS

PCI DSS is the foundation of payment security and outlines key requirements for encrypting sensitive data, securing your networks, monitoring and limiting access to information, and regularly testing your systems. PCI DSS also divides merchants into four categories based on transaction volume, with each category subject to a differing degree of strictness.

PSD2

Applicable in the EU, PSD2 requires strong customer authentication and secure communication standards, shaping how each payment gateway interacts with banks and third-party providers.

KYC/AML

It is critical to verify user identity and monitor suspicious activity at all steps in the payment process and within all payment gateway functions. A payment gateway must support automated KYC, AML checks, and ideally, perform continuous risk scoring.

Security best practices

- Implement tokenisation and strong encryption mechanisms

- Define your fraud detection rules and logic

- Build and maintain detailed audit logs

- Monitor transaction in real-time to prevent breaches

Data privacy and cross-border compliance

Global payment gateway operations must follow regional data laws and implement geographic controls on data storage and transfers.

General data protection regulation

GDPR defines how a payment gateway must process, store, and protect EU consumer data, with strict consent and retention requirements designed to keep both merchants and consumers safe.

Conclusion and next steps

If you have an enterprise-level budget and the necessary resources to create online payment gateways, then building in-house may be the next best step for your business.

However, if you need to accept payments fast with minimal risks and compliance burdens, a provider like payabl. can give you everything you need to integrate an optimised payment gateway that makes money move seamlessly and efficiently.

Not sure what solution is right for you? Schedule a consultation with payabl. today.

FAQ

How much does it cost to develop a payment gateway?

Exact figures vary but to build a payment gateway from scratch can cost anywhere between €1,000,000 and €10,000,000.

What is the future of payment gateways?

Providers like payabl. offer payment gateway services designed for a better future of payments security and efficiency.

Can I start my own payment processing company?

Yes, you can start your own payment processing company, but it requires significant capital, large and dedicated teams, strict regulatory licensing, bank partnerships, and a high level of technical expertise.

How are payment gateways built?

Payment gateways are built using secure architectures and frameworks, with core transaction-handling modules and integrations with financial institutions. Building a payment gateway requires compliance with strict regulations that can add on to development costs.

Can I develop my own payment gateway?

Yes, but for most businesses, it is generally more cost-effective to opt for a pre-built or hybrid payment gateway that comes with outsourced technology and support.